As week 3 of the war on Iran draws to a close, it has been confusion and contradiction. The End game? There isn’t one! Iran is proving highly resilient and continues to launch targeted strikes across the region. There’s no evidence its stockpiles of missiles, rockets and drones are close to depletion. This week its strike on Qatar’s Ras Laffan LNG terminal – in direct response to Israeli strikes on Iran’s South Pars NG processing facility – triggered a sharp spike in energy prices. You can sense confusion and mixed messaging among the allies. Even Trump is now calling for de-escalation. This week, his Head of Counterterrorism (Joe Kent, an ardent Trump supporter) resigned saying Trump had been misled about the threat Iran posed and blamed media and high-ranking Israeli officials & lobbyists. The US is now even considering lifting sanctions on some Iranian oil. Why? Because inflation pressures are already starting to bite and the latest energy price spikes will make it even worse. There are serious question marks just how far the US and Israel are aligned following Israel’s attacks on Iran’s South Pars gas field. Trump claims he knew nothing about Israel’s plans. Initially, Israel claimed otherwise but then yesterday Netanyahu confirmed Israel “acted alone”. In a news conference yesterday, PM Netanyahu said “Iran no longer has the capacity to enrich uranium or make ballistic missiles….we are winning and Iran is being decimated”.

So, where does all this leave things?

-

- President Trump has publicly appealed to allies to help secure the Strait of Hormuz: These calls have largely been rebuffed.

- The Strait of Hormuz has become the central pressure point: Iran wants to control access – and is succeeding. Shipping volumes are almost at a standstill. The result is energy markets are pricing geopolitical risk directly.

- Shift in language: The original framing for the war was “regime change”. Now it’s to secure shipping lanes and de-escalate. There has been a clear downgrade in the messaging. Duration creep is setting in (i.e. this war will be “over very quickly” to one lasting weeks, even months).

- Gulf States no longer look like safe havens: The UAE – long-viewed as a regional oasis – has come under sustained missile and drone attacks; the perception of geopolitical stability in the region has been materially undermined. Iran has shown it can reach all corners of the regions. The likelihood of them joining the war is extremely low – imagine what will happen to oil prices. It will be the 1970s all over again!

- Modern warfare has been fundamentally redefined: Low-cost drones ($20k–$30k each) can be mass-produced and deployed at scale; Interceptors cost millions and struggle against swarm tactics; Decoy drones ($10k each) further complicate defences; the result is cost asymmetry has turned decisively in favour of the “smaller, nimbler guy”.

- Geopolitical contradictions are quite explicit: The US is (1) implicitly allowing increased Russian oil flows (as part of a sanctions waiver), (2) considering lifting sanctions on some Iranian oil, (3) trying to avoid strikes on energy infrastructure to help stabilise markets and (4) turning to Ukraine for drone expertise. The irony is remarkable – in effect, a transactional approach to alliances where one adversary is being used to offset another – all so that consumers don’t feel the pinch in their energy bills.

- Macro and Political Spillovers: Oil and inflation dynamics are now front and centre. Energy has become the primary transmission mechanism into the global economy; the key question is how persistent it remains, hence today’s caption!

- US domestic political risk is rising: The Republican Party faces potential (and perhaps large) losses in the upcoming mid-term elections in both Houses; this risks turning Trump into a lame-duck president.

- AI might prove to be a counterbalance — but only with consequences: faster AI adoption could offset inflationary pressures via productivity gains but with potential labour market disruption (upending the current “low hiring, low firing” balance); if so, this would result in social strains. Look at the speed and impact of AI on existing technologies and the knock-on effect into the world of private capital.

- Global growth will become increasingly polarised: Economies will become correlated to Hormuz-linked energy flows and the wider, energy markets. There will be a divergence between energy-secure and energy-exposed economies.

- For markets, we have witnessed a see-saw effect: some of 2026’s worst-performers (software, crypto) have rebounded since the strikes on Iran. The war has interrupted the dominant AI-disruption narrative thus enabling the likes of software to recover. This is tactical – not structural. Markets are not reacting to the war itself – they are reacting to how long energy prices remain elevated.

Below is a projected timeline. The yellow section denotes where we are now – the “Persistence Test”. Key takeaways, for those calling themselves Asset Allocators, are (1) under 4 weeks, the shock is manageable; (2) between 4 to 12 weeks sees policy friction (i.e. when it becomes a Central Bank problem because inflation is rising – or at least not falling – and growth is weakening; CBs cannot satisfy both objectives at the same time); (3) between 3 to 6 months, you have macro regime risk (i.e. changes start to become structural/embedded – no longer temporary) and (4) over 6 months results in systemic consequences.

| Phase | Timeline | What Matters | Oil Dynamics | Inflation Impact | Policy / Rates | Market Behaviour |

| 1. Shock & Transmission | 0–2 weeks | Initial escalation, headlines, liquidity | Spike driven by risk premium; highly volatile | Expectations rise; no CPI impact yet | Central banks pause; watch mode | Risk-off bursts; USD ↑; yields ↑; equities volatile; flows to cash |

| 2. Persistence Test | 2–6 weeks | Whether oil remains elevated | Stabilises in $90–100 range | Fuel feeds into CPI; disinflation slows | Rate cuts delayed; curve flattens | Rotation begins; Energy/Defence ↑; cyclicals ↓; credit starts widening |

| 3. Policy Friction (see explanation above) | 2–3 months | Inflation becomes visible | Sustained $90–110 critical range | +0.3 to +0.7pp; early second-round effects | More hawkish tone; real yields rise | Multiples compress; quality outperforms; HY/EM weaken; gold firms |

| 4. Macro Regime Shift (see explanation above) | 3–6 months | Duration of shock | Sustained $100+ | +0.7 to 1.5pp; core inflation risk | Cuts delayed materially; tighter conditions | Broad risk-off; earnings downgraded; credit widens; commodities outperform |

| 5. System Stress / Resolution | 6–12 months | Endgame (resolution vs escalation) | $120+ = stagflation risk | Inflation entrenches; expectations at risk | Policy dilemma (growth vs inflation) | Either stagflation (risk ↓, gold ↑) or sharp relief rally |

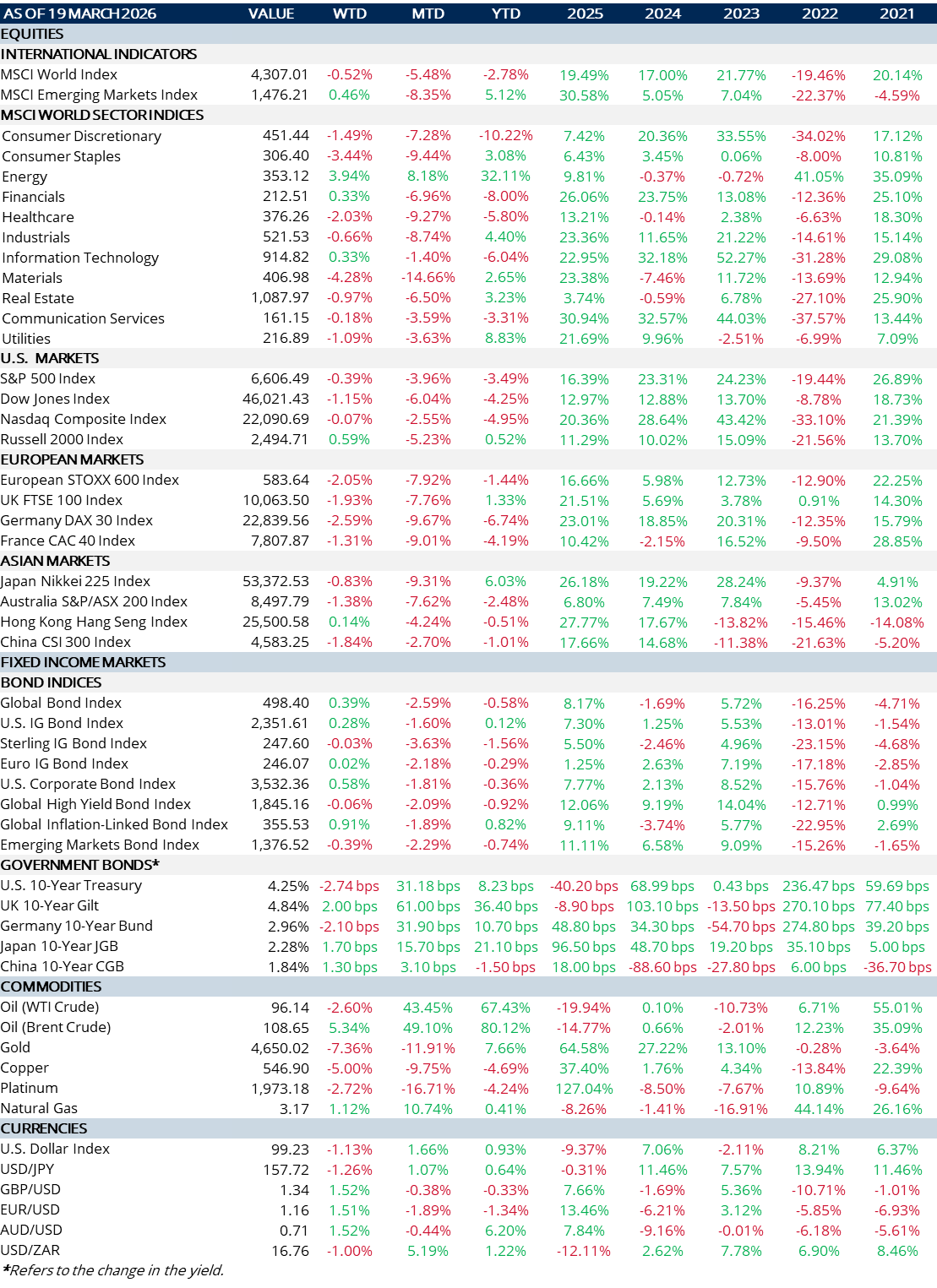

MARKET SUMMARY...

-

- The Fed left rates unchanged. It was unanimous, only one dissenter – Stephen Miran (as expected). Target range remains 3.5% to 3.75%.

-

- Other CBs: BoE left rates unchanged at 3.75%; SNB held rates at 0%.

-

- Projections for US inflation by end-2026: Headline rate 2.7% (from 2.4%); Core rate 2.7% (from 2.5%); 2% target will not be hit till 2028.

-

- The Dot-plot (rate projections by the 19 FOMC members, end-2026): 7 see no change; 7 see one cut; 2 see two cuts; 2 see three cuts; 1 see four cuts!

-

- Gold and Silver are still selling off as inflation fears grip markets.

-

- Bond yields (2y through to 30y) remain elevated globally pressuring budgets even more as interest-servicing keeps rising.

-

- The table below speaks volumes – a sea of red with only energy being the winner.