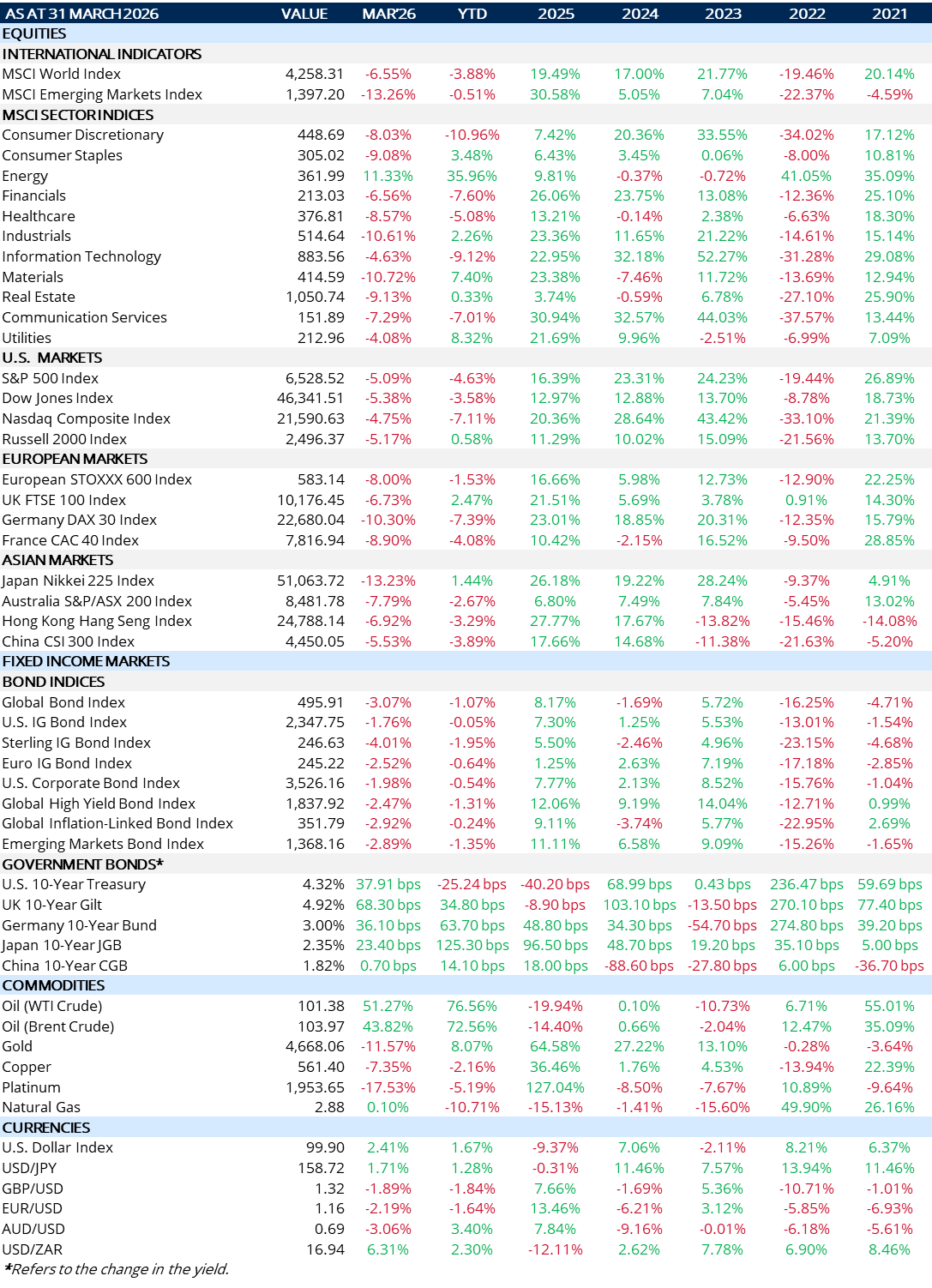

Q1 is over and it has been nothing short of eventful. Geopolitics and ensuing volatility dominated throughout. The drivers are clear as covered in my four, previous weeklies. The table below sets out March performance and where all this leaves us on the year. The key question now: what is the Outlook for Q2? Below are some of the key factors shaping the outcome:

Will the US stay or pull away?

There are clear signs of fatigue setting in at different levels. The US’ actual positioning is one of deterrence and containment while public signalling is clearly one of de-escalation/negotiation. The latter has been a key reason for markets staging a rally these past couple of days. Strategically, the US can’t fully withdraw for credibility reasons as well as the dependency Gulf states and Israel have on the US. The energy security issue at stake is global – not domestic. Its stance is more likely to be one of “managed containment” – which might explain the total deployment of some 60,000 troops in the region.

What is Iran’s optimal strategy?

In a nutshell, controlled instability – and it has been doing this very well! It wants to continue maximising oil risk premium while avoiding full-scale retaliation. The former hurts importers (allies of the US) while also raising its leverage; the latter destroys infrastructure – including Iran’s. They are restricting throughput without full closure, creating ambiguity and insurance risk and weaponizing uncertainty. Peace à oil price collapse; outright war à regime risk. Bluntly: this is asymmetric warfare applied to commodities.

The impact of high and rising energy prices on global budgets?

Let’s not kid ourselves – it’s already hurting! Both oils (Brent and Crude) are up some +50% in March. In the US, gasoline is +33%. Rising energy costs are having a direct, transmission effect (aka first-order effect) as follows:

- Airlines are cutting routes

- Airfares – especially routes to/from Asia – have increased materially

- Logistics companies (e.g. FedEx, USPS) are adding surcharges

- The likes of 3M are facing industrial pricing pressure

- Households are finding travel more expensive, goods inflation rising and confidence is falling

- Government bond yields have soared (e.g. in the UK yields are above 5% and have eroded the Chancellor’s fiscal headroom by some £5bn)

- In Emerging markets, fuel rationing is already underway

The second-order (indirect) transmission effect (the amplifier effect) is impacting fertiliser (+50%) which will hit food prices, creating aluminium shortages (resulting in an industrial squeeze) and a risk to Helium supplies (important in semiconductor disruption). Basically, we move from oil inflation à system-wide cost inflation.

What about Gold?

We witnessed the sale of gold by Turkey’s central bank (one of the big, EM buyers). Was this a one-off or something systemic? Still early days but it might not be a one-off – rather the first crack in the system:

- Turkey sold/swapped $8bn of gold in two weeks. It was driven by currency pressure (the TLira is highly volatile) and an ever-rising energy import bill

- Mechanism: energy importers need US$ to pay for the energy à leads to a US$ shortage à sell gold to create the liquidity

- The broader implication is a slowdown in central bank gold accumulation – even outright sales if the crisis persists. Interestingly, it’s as if the narrative has been flipped: central banks have gone from structural gold buyers (“safe haven”) to forced sellers (“gold = liquidity collateral”).

- Whether this persists really depends on the future direction of this war!

What about Equity/Sector moves?

The fallers are fairly obvious (some have been referenced above):

- Airlines (fuel cost shock)

- Logistics/Delivery (margin squeeze)

- Consumer Discretionary (demand & cost hit)

- Packaging/Chemicals (Input inflation)

- Europe/UK (energy sensitivity)

The winners? Fertiliser stocks, Plastics, Energy and US commodity-linked producers.

Summing up:

- Are there buying opportunities? Not really – but they are building; things are cheap – but the likelihood is they need to get cheaper. Don’t forget markets are – give or take – only some 8% off their highs! That’s not a lot in the grand scheme of things. The capitulation stage is not really upon us yet – as I mentioned above, Iran has the leverage and the US can’t just walk away! Liquidity is still functioning – wait till it hits a clear bottom and then it will be time to buy.

- What looks interesting – but still too early? SaaS (Software-as-a-Service): Investors have aggressively priced in the idea that AI will reduce demand for SaaS, compress pricing and increase competition. So, the market has pre-emptively repriced SaaS stocks as if this is already happening. We have seen multiples down, growth assumptions cut and some names (e.g. Salesforce, PayPal) trading at “no-growth” valuations. In other words, the market has frontloaded the bad news. If the market is right then AI destroys pricing power of SaaS. If not, SaaS is undervalued. The Payments sector looks interesting. Well-known names have been hit hard and are even priced for zero/negative growth. Another area some Consumer Staples – these are a defensive, stable & reliable play valuations have been hit hard.

- This is a valuation reset, not structural collapse. However, buyer beware, macro pressures haven’t finished repricing it all yet. It’s not about whether the conflict escalates – it’s about how long the pressure is maintained!

MARKET SUMMARY...

- The big unknown is the path of interest rates. Since the start of the Middle-East conflict, volatility has been driven mainly by the hawkish tone of central banks i.e. no change/possible rate rises. Implied volatilities have risen across assets because of this uncertainty. We’re now seeing signs of moderation for one of three reasons: (1) Growth prospects are dimming; (2) De-escalation prospects are rising or (3) it’s dawning on CBs keeping rates the same, let alone raise them, will be a double-whammy for consumers.