Last Friday (20th), the Supreme Court Of The US (SCOTUS) struck down President Trump’s use of his IEEPA (International Emergency Economic Powers Act) on the grounds he exceeded his Presidential authority. So, instead, the Administration shifted its legal strategy to s122 of the trade Act 1974 – which provides a narrow, time-limited emergency authority with a hard, statutory cap. Following the SCOTUS announcement – which, quite frankly, the Administration had anticipated and was prepped for – an initial 10% was announced under s122 (on 20th Feb.), swiftly followed by an increase to 15% the next day.

The three most important takeaways of this decision are:

- Tariffs are now legally temporary and, unlike the IEEPA tariffs, can only remain in force for 150 days under s.122 after which Congressional approval is required.

- Congress is truly back in the game and, with the mid-terms coming up in November, could get stronger. Trump needs some luck if the tide is going to turn back in his favour.

- Trump’s ability to “shock-and-leverage” is now time-limited!

Implications on existing trade deals? The move to a blanket 15% rate creates significant friction with countries that had previously negotiated lower rates under IEEPA:

- UK and EU Status: Many U.S. allies, including the UK and the EU, previously had deals for lower reciprocal rates (e.g. 10%). These countries will now face a higher 15% global tariff under s122 vs before.

- UK Impact: The BCC (British Chamber of Commerce) has estimated this extra 5% increase could raise costs on UK exports to the U.S. by as much as ?3 billion.

- Exemptions: Some categories will continue to remain exempt (e.g. certain, critical minerals, pharmaceuticals, fertilizers and some agricultural products). Canada and Mexico also retain most of their exemptions under the USMCA pact.

Then there’s the matter of an estimated $180 Billion collected in tariffs over the past year and, potentially, how it is refunded! Trump has indicated refunds will not be given without a legal battle. If so, this “could take years”. Knowing this, most corporates will likely provision conservatively. They are more likely to be “grateful” the decision has been overturned and to leave it at that. The SCOTUS ruling – which affects approx. 75% of the total tariffs Trump enacted last year – means the Effective Tariff Rate (ETR) drops to about 13.7%. Previously, it was about 15%. Furthermore, if after 150 days Congress does not endorse it, the tariff expires in which case the ETR drops even further to about 9% – still higher than before the start of Trump’s second term but significantly less vs where it was. The 75% group relates to all the IEEPA tariffs (i.e. those announced on “Liberation Day”, the 10% China fentanyl-related tariffs and the 25% to 35% tariffs on Canada and Mexico). The remaining 25% relates to non-IEEPA tariffs that were imposed under different laws and these remain in place (these include the 50% on Steel, 50% on Aluminium and 25% on Autos as well as the s301 tariffs on unfair trade practices).

Market implications?

For markets, this ruling is less about what it removes today; it’s more about how it alters (1) expectations going forward, (2) bargaining power (i.e. leverage) and (3) timelines. Tariffs themselves have not disappeared – it’s their perceived state of permanence that has. They have gone from open-ended to time-ended and this is a key distinction because markets are all about clarity and timing. In this regard, there is a clear chain of events: Inflation expectations, Rates (front vs long-end yields), US$ impact, Equities, Reaction of trade partners and Political Path:

| Channel | What Has Structurally Changed | Immediate Market Interpretation | Market Reaction (So Far) | Portfolio Considerations |

| Inflation Expectations | Tariffs still at 15% but legally for only 150 days. Persistence risk reduced | Inflation still present near term – but medium-term tail risk is reduced. | Breakeven rates roughly stable; no immediate repricing pressure. | Positive: Duration-sensitive equities (Growth, Quality).

Negative: Pure inflation hedges; select Commodities. |

| Yield Curve Impact (Front-End, Long-End & Curve Shape) | S122 means Congress caps any policy escalation; credibility around inflation improves. | Lessens pressure for aggressive repricing – Yield Curve less likely to steepen meaningfully. | Yields remain rangebound; Yield Curve modestly flatter. | Positive: Utilities, Infrastructure, Insurers, Quality Financials.

Negative: Highly levered cyclicals, aggressive curve steepener strategies. |

| US$ | US$ strength less structurally supported as rate pressure has lessened. | Support has shifted from structural to tactical. | Steady – no breakout in sight. | Positive: EM assets, Non-US equities.

Negative: Defensives, exporters. |

| Equities (Broad & Sector) | Reduced uncertainty; focus now on timelines and negotiation. | Move from Index-level Risk-Off to Rotation. | Indices rangebound; volatility still prevalent; sector dispersion continues. | Positive: Defence, Domestic Services, Select Industrials.

Negative: Import-heavy retail, low-margin manufacturers; legacy software. |

| Credit (IG & HY) | Escalation risk reduced but issuance remains heavy as does growth uncertainty. | Selective Carry trades still attractive. | Slight but orderly widening in IG spreads; HY under more pressure. | Positive: Financials, Euro Banks, High-quality short-duration IG.

Negative: Long-dated low-spread IG. |

| Trade Partner Reaction | Negotiation leverage shifts from “shock” to bargaining; the “middle powers” will accelerate efforts to diversify their supply chains; greater attempt at realigning with trade bodies (e.g. CPTPP-EU). | Retaliation risk reduced but we’ll see a new round of interim deals; China will delay its response; the US-centric trade architecture will erode. | Not seen any immediate retaliation from countries yet; FX scene has been muted; diplomatic engagement is accelerating. | Positive: ASEAN industrials; EU-Asia trade facilitators.

Negative: US centric exporters. |

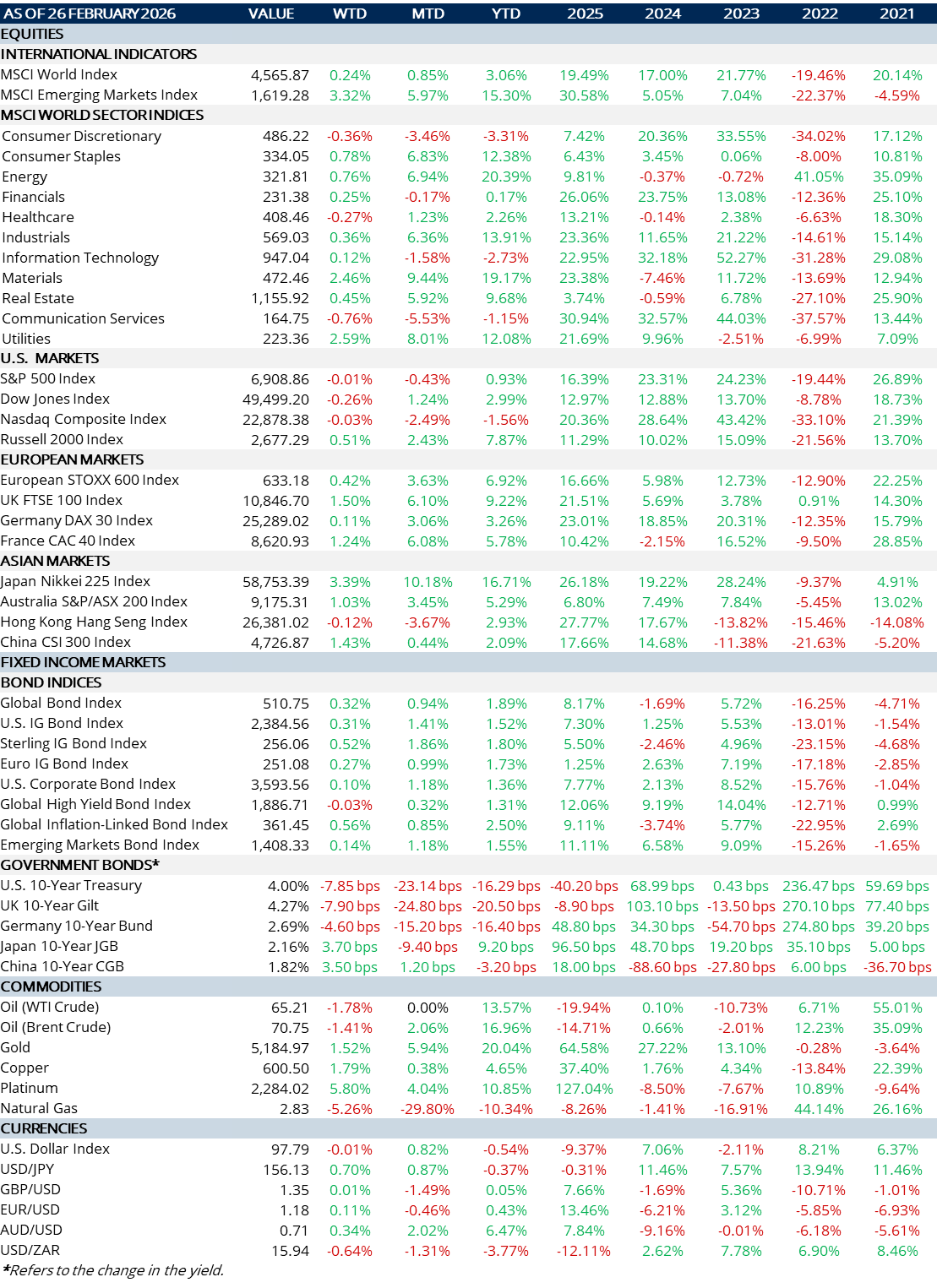

MARKET SUMMARY...

- US Treasury yields are little changed – even in light of the above.

- UK saw the Labour party heavily defeated in the Denton and Gorton by-election. Turnout was poor (47.5%) and little changed vs the general election in 2024….but unlikely Starmer will be going. Markets have priced the bad news (that we know of) including the upcoming council elections. Gilts have continued their outperformance as more rate cuts are expected.

- Japan latest inflation (CPI) print (1.6% y/y) remains below the BoJ policy target (2.0% y/y). Equities continue to perform strongly.

- Credit markets remain flustered off the back of AI and lately private debt concerns.