On Thursday this week, President Trump will be bringing many members of its “belt of US-convened” (as opposed to US-aligned) states from across Eurasia to Washington for its inaugural “Board of Peace” meeting. This “Board of Peace” comprises some 27 signatories and spans across Central Asia, the South Caucasus, greater Black Sea Basin and adjacent regions of the Middle East and South Asia. It has been labelled a “Big Beautiful Belt” (BBB) – a variation on his OBBB (One Big Beautiful Bill). It’s another clear signal how global power is now being exercised – less via ideology but, instead, more through trade routes, corridors and optionality! The timing is no coincidence either: it is aimed directly at China’s BRI programme (Belts and Roads Initiative). The differences between the two lies in the detail and their modus operandi. The table below compares and contrasts the two:

| Dimension | China – Belt and Road Initiative (BRI) | United States – “Big Beautiful Belt” (BBB) |

| Methodology | State-driven, capital-led infrastructure and connectivity programme. | Looser, coalition-based framework of connectivity & security. |

| Core strategic aim | Lock in long-term trade and energy routes. | Dilute China’s corridor dominance without direct confrontation. |

| Focus | Ports, rail, energy, pipelines and digital networks. | Corridors, logistics and routing options. |

| Financing | Loans/debt provided via policy banks, executed by SOEs. | Not clear but likely a blend of: Public-Private financing via Allies, DFIs and Multilateral Partners. US funding unlikely to be significant (unless part of a Trumpian style deal!). |

| Geographic risk management | Reduce vulnerability to maritime chokepoints (e.g. Malacca). | Reduce reliance on Russia- and Iran-linked transit routes. |

| Power projection method | Extend political influence via infrastructure dependence. | Shape behaviour by providing alternatives and exit optionality. |

| Economic architecture | Embed Chinese standards, contractors and financing norms. | Avoid ownership; facilitate corridors and partner-led execution. |

| Security burden | Implicitly retained by China via control and leverage. | Explicitly shifted to regional partners. |

| Dependency profile | Encourages long-duration structural dependence. | Designed to minimise dependence and preserve strategic exit options. |

| Strategic philosophy | Control and lock-in. | Flexibility and denial. |

This naturally comes on to the next question: what are the timelines? Bear in mind Trump’s Presidency only has 3 years to run assuming no Government paralysis (e.g. a very poor mid-term election outcome that impedes progress). Three factors will influence timelines:

- Institutional establishment (i.e. the legal, membership and governance framework).

- Financing mechanism (i.e. ideally, repeatable funding channels combined with a project pipeline).

- Logistics (i.e. the physical reality of moving meaningful volumes – this means ports/pipelines/rail networks would have to be operating at scale).

With the above in mind, the table below compares how long it took BRI to reach its present status vs how long it might take BBB (based on what’s known, what’s plausible and what would count as established):

BRI |

BBB |

|

| Institutional | 1–3 years (2013 – 2016). Originally announced in Sep. 2013 (“One Belt, One Road” initiative before changing name to BRI); today, 148 countries have signed MoUs with China to trade on five pillars including investment, trade & people exchanges. | Months (Jan/Feb 2026) This is all about formal existence – it does not speak to effectiveness. There is no treaty, bank or financing in place. It’s creating a brand – substance is to follow (if at all). |

| Financing model | 3–7 years (matures mid/late 2010s). To date, China is the largest sovereign lender with over $1.5tn in investment (via loans and credits). The bulk has gone towards traditional infrastructure. In doing so, it promotes the internationalisation of the Renminbi (RMB became the fifth most-traded FX globally as of July 2023). | 1–3 years if DFIs/allies/private capital platform becomes real (not proven yet) |

| Physical reality | 10–20 years as a system. BRI was never a single programme. Instead, it is a layered, compounding network. The 10-20 years reflects sequencing of mega-projects, network effects (port+rail+customs integration+industry) and political negotiation cycles. | 2–8+ years for meaningful corridor effect; out to around 2030 for step-change scale. The China BRI speaks to time – even though the BBB is an abbreviated version of BRI. |

In a nutshell, BRI is all about who owns the roads – BBB is about making sure no one road ever matters too much over another! From a market perspective, that’s how pricing will differentiate one from the other. This has key implications for portfolio management as a distinction must be drawn between liquid investing (i.e. quoted) and illiquid investing (which effectively amounts to Real Asset investing). The table below looks at winners and losers with liquidity in mind:

| Dimension | Winners / Overweights | Portfolio Management consideration(s) | Liquidity Profile |

| Equities | Logistics & trade-facilitation operators; defence & security tech | Operators and enablers outperform builders; throughput > concrete | Mostly LIQUID(listed equities, ETFs) |

| Fixed Income | Corridor sovereigns (Central Asia, Caucasus, Turkey, select Gulf countries). The more “swing”, the better! | Optionality premium tightens spreads ahead of fundamentals | LIQUID to SEMI-LIQUID (sovereigns, hard-currency debt) |

| Commodities | Uranium, copper, critical minerals with secure/friendly routing | Routing security increasingly priced alongside supply | LIQUID (futures, large producers) |

| FX | Corridor currencies benefiting from transit, fees and capital inflows | Route concentration risk now FX-relevant | LIQUID(spot/forwards) |

| EM Allocation | Corridor EM equities; EM logistics operators; EM resource exporters | EM alpha shifts toward optionality and resilience | LIQUID (public markets) |

| DM Allocation | Defence/security tech; logistics software and services | DM exposure via services and security, not bricks | LIQUID |

| Private Infrastructure | Select ports, rail bottlenecks, logistics hubs on Middle Corridor | Value in bottlenecks, not monuments | ILLIQUID |

| Private Credit / PPPs | Blended-finance corridor assets | Credit risk improves where optionality exists | ILLIQUID |

| Stress test: Trump loses the House | Core corridor trades intact | Pace slows; thesis survives | Liquid assets adjust faster |

| Stress test: China stimulus resurgence | Tactical China beta; commodities | Noise rises; long-term competition intensifies | Liquidity favours agility |

MARKET SUMMARY...

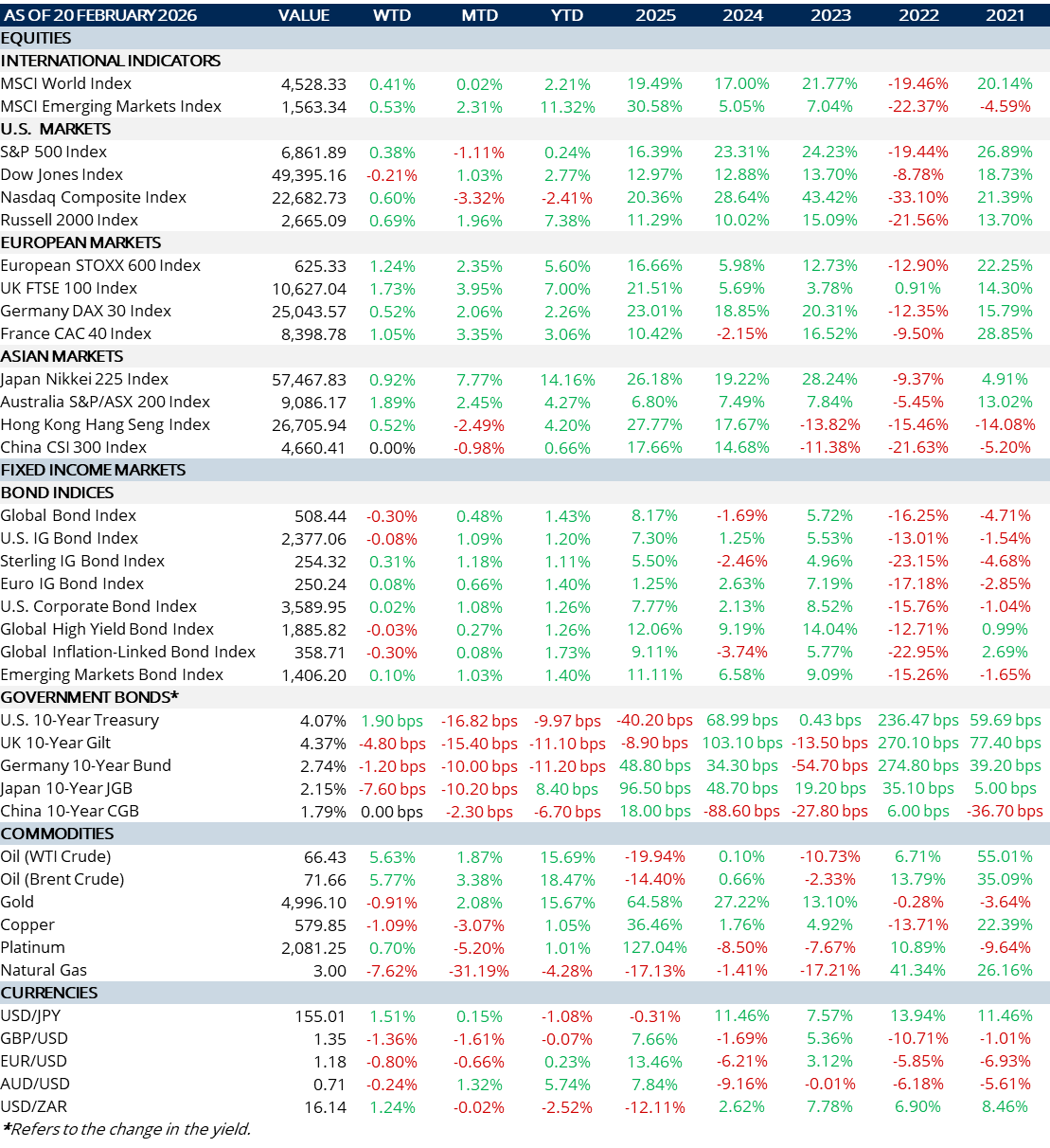

- US yields remain rangebound while the yield curve continues to flatten (from the short end); the Fed remains “comfortable” where rates are vs the economy. Curve steepening will only happen if aggressive rate cuts come back into play – and latest FOMC minutes do not point to this. Two rate cuts remains the forecast for 2026. $2tn has been wiped off Enterprise Software valuations on the back of fears AI can rapidly displace non-manual labour. Latest revelations around Blue Owl Capital will be one to watch! The latter has permanently restricted withdrawals from one of its retail-focused debt funds and this is fuelling fears about the alleged private credit bubble. This was after selling off some $1.4bn of loan assets held in three of its private debt funds.

- In the EuroZone, the inflation and bond outlook is softer than the US. Bunds are still rangebound (due to spending on defence and bond supply). ECB head Christine Lagarde wants out early – probably with her sights on the French Presidency.

- In Japan, long-dated bonds (JGBs) outperformed over suggested changes to accounting policy which eased selling pressure. Inflation sits below the BoJ’s target aided by lower food price pressure. Two hikes are expected this year.

- Oil prices remain elevated on rising US-Iran tensions.