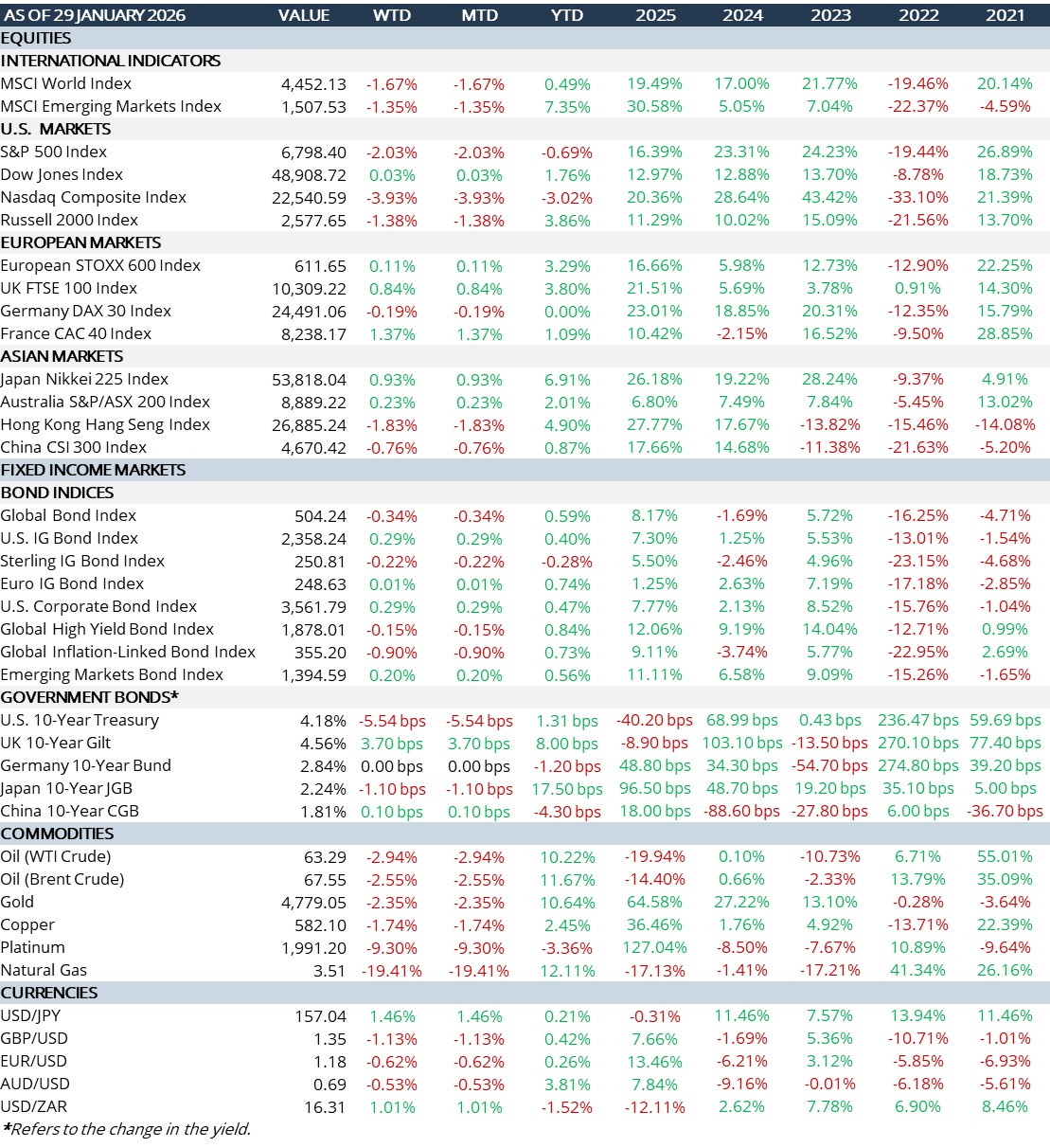

January is already over. Had you been away on holiday and returned at month-end, you would be forgiven for thinking everything looked fine – just another, “up” month. Look at the table below of returns for a sample of asset classes, in US$:

Volatility catalysts were plenty (Venezuela, Iran, Greenland, new Fed Chair) – yet most major asset classes finished in positive territory. However, it would have felt very different if you were living through it. Gold and Silver experienced major pullbacks following a significant runup. It’s always a “chicken-egg” situation. Few investors can handle too much of a good thing. Inevitably, they start “looking” for a reason to pull back….and there were several catalysts in play towards the very end of the month that triggered big moves in different asset classes – and not all were favourable:

- Trump’s response to the US$ declining was: “No, I think it’s great”. It fell against almost every major G10 currency while the US$ Index had its worst 4-day slide.

- The new Fed nomination surprised markets – Kevin Warsh, considered a hawk and one who keeps a watchful eye on inflation. After all the grief Trump gave Powell, markets were quite confused by this announcement as it seems to go against the grain of what Trump wanted. This meant the US$ “debasement” trade was being questioned.

- Oil was boosted by the threat of substantial US military and troop movement in the Middle East around growing uprisings in Iran with so many civilians being killed.

- Japan’s market rallied hard on the announcement of snap elections to be held this coming Sunday (8th). All parties are pledging consumption tax cuts. 10y and 30y bond yields shot higher (i.e. bond prices fell).

The nomination of Kevin Warsh as the new Fed Chair was perhaps the most important, late-month development. The obvious question: does he know what he’s in for under Trump? Warsh is a former Fed Governor. He also worked on Wall Street and in the White House (under George W. Bush) so he knows how the machine works. He has also been a strong advocate for reforming the Fed. He openly criticised the QE (Quantitative Easing) post the GFC (Global Financial Crisis) as well as the two rounds of QE before and after Covid. He argues this has made the economy weaker over time. His nomination is still to be approved by the Senate Committee. Many point to his appointment as the key trigger for the selloff in precious metals. Why? Here’s where the paradox lies: Trump wants lower rates while Warsh is seen as an inflation hawk. So how does that work? Warsh’ recent comments/statements have actually indicated a desire to cut rates citing AI-driven productivity growth as a strong deflationary force. Is he right? The theory of AI-driven productivity certainly is. To my mind, it has been the primary driver of the slowdown in the job market in recent months. In turn, it should allow him to relax monetary policy while still managing to keep inflation on hold. Despite this, can he still shrink the Fed’s balance sheet albeit in a more relaxed way? This is the big debate…..banks are reaching their low-end in reserves. This matters because if he overdoes it on further balance sheet reduction, he seriously risks tightening financial conditions even more……however unintentional! Besides cosmetic changes, the Fed will be hard-pushed to shrink the balance sheet further if it is to maintain domestic liquidity levels. We should find out quite quickly.

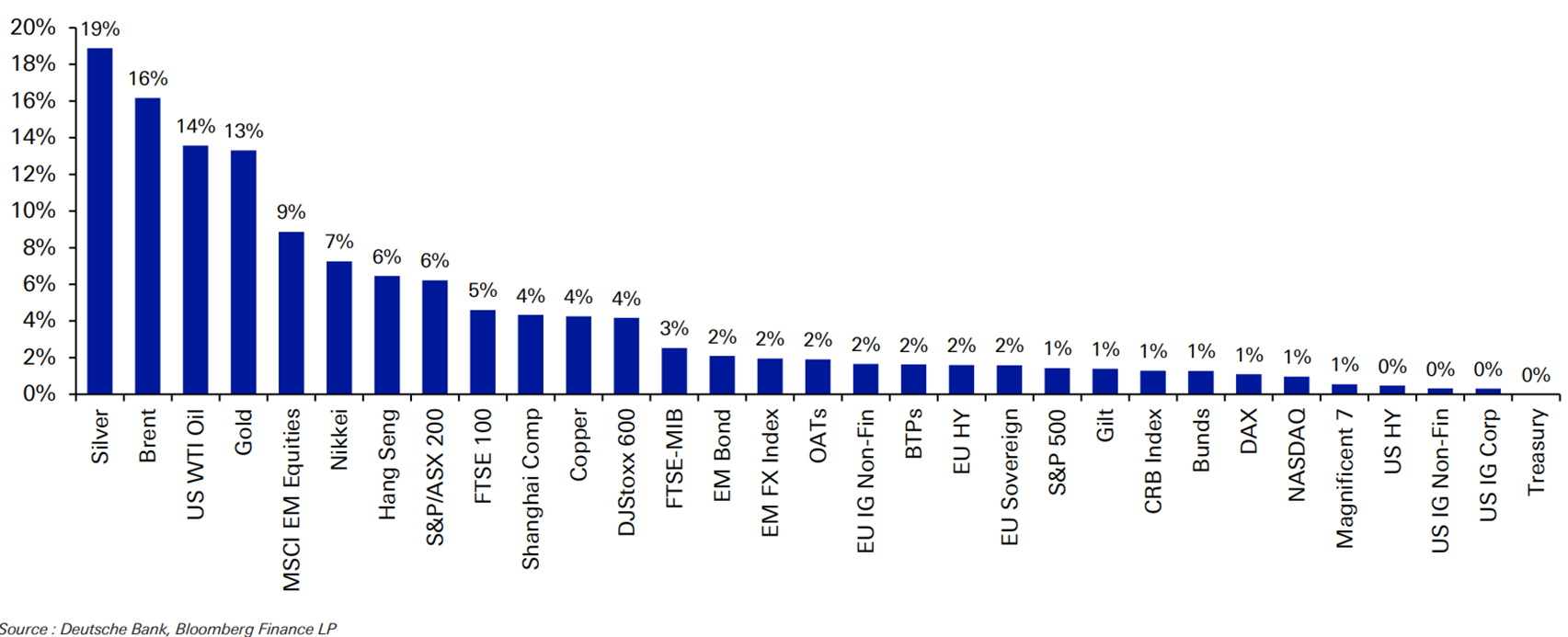

Precious metals? The last two working days of January saw gold fall some 10% while silver sunk 16%. This downward move has extended into February:

- One catalyst (see above) was the nomination of Warsh as the next Fed Chair.

- A rally that was clearly overextended then saw geopolitical risk premium reduce on the back of easing tensions between the US & Iran.

- Major exchanges (e.g. CME Group) raised margin requirements for gold and silver thus forcing speculators to close out leveraged positions to avoid higher collateral costs. As an example, the initial margin required on a 5,000/oz contract has jumped from up to $25,000 to $32,500 making a 62.5% increase! Shorting also faces higher margins – compounded by the difficulty in sourcing metal as futures settlement approaches.

- While China has not banned silver exports outright, they have reclassified it as strategic commodity. The outflow of all silver is controlled through 44 licensed companies – so each ton of outbound silver is now additionally a political decision, no longer just a price decision.

- Big losses were racked up by Chinese metal traders totalling some $140m+. It is believed one of the traders’ counterparties fled the country leaving deals unfinished. The episode involved an intricate network and involved was a state-backed entity (SDIC). Another trader – who made a fortune riding gold’s ascent (estimated at $3bn) – has now place a huge bet against silver which stands at 450 tons (= 30,000 contracts). The drop in silver’s price last week is estimated to have netted him close to $300m. since then, silver has fallen a further 16%!

So, all-in-all, it was the perfect storm…..but it does raise the question was this a fundamental correction or a technical one? I think it leans very heavily to the latter as technical traders (Algorithmic, Day-traders, Systematic, CTAs and the Speculator community at large) dominate market positioning – further compounded by use of leverage (margining and derivatives).

…..and what about Tech/AI? The other rout going on at the same time as metals is the sell-off in AI. In just a couple of days, several hundred billion has been wiped off the value across anything to do with Silicon Valley. It’s difficult to pinpoint one, specific factor but, rather like metals, seems to be a confluence of several that have fuelled investor fears:

- Something that has been labelled “SaaS-pocalypse” is about how new AI tools can substitute faster than incumbent drivers can defend themselves when it comes to high-margin enterprise software / information services. In other words, AI is surpassing existing tools. Traditional “Software-as-a-Service” is being sold off.

- This same sell-off is taking place across equity and credit (public and private). Credit and equities are like gold and silver – when one (credit/gold) start wobbling, the other (equities/silver) start repricing even faster!

- A lot of private credit money has gone into AI buildout via structures (private credit, loans, CRE/Data Centre finance). This raises long-held concerns over pricing and transparency.

Software/services are seeing the biggest bleed because investors are trying to reconcile two different things at once: AI making legacy software obsolete vs AI spend still remaining huge and durable. Until investors can decide what the new balance is, we continue to see a violent selloff. What happens next? You either get a sharp rebound once a clearer picture emerges around revenue or multiples compress further and suddenly the pain extends beyond selloffs and results in downgrades and refinancing stress! The next clues will be in what company officers have to say on earnings calls, how credit spreads (a measure of risk) move and how deep AI Agentic tools reach (i.e. will they displace existing spend or drive new spend?).

MARKET SUMMARY...

- Overall, a stormy week for markets driven by the above, two factors.

- Economic data continues to be robust – supportive of stable economies, not collapsing ones.

- Europe was lacklustre over the week – ECB kept rates on hold.

- Japan goes to the polls this Sunday. Forecasters predict a strong win for the LDP, even an outright majority. Meanwhile, inflation is dropping – welcome news for PM Takaichi.

- The UK is embroiled in uncertainty – PM Starmer’s position is the most precarious it has ever been. The GB£ has taken a knock because of it and bond yields are up (i.e. bond prices are down).

- As discussed above, software stocks have been hammered. People are now waking up to the powerful contribution of Gen-AI on the rest of the software industry.