Japan’s bond market has, for a long time, been the global outlier when it comes to demonstrating stability. Now, rather abruptly, it has become a source of volatility. This is not simply a rates story. It suddenly finds itself playing the role of a normal, high-debt sovereign – something it has not been used to as it now battle with fiscal credibility, the profile of its bond buyers and how its Central Bank (the BoJ) responds.

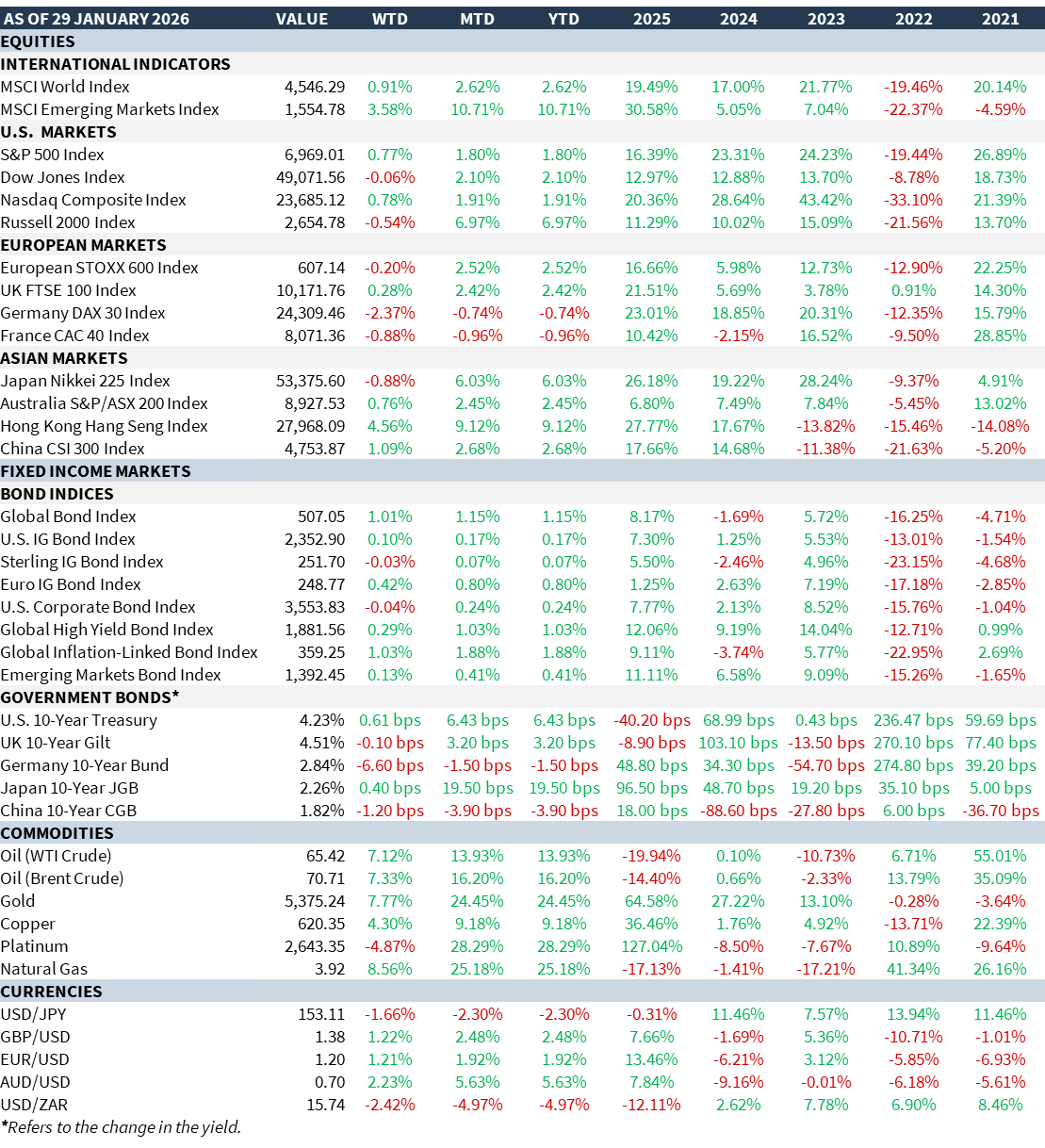

In January, Japanese government bonds sold off aggressively. The 10-year yield breached 2.2% reaching a 27-year high while the 20y and 30y yields rose to 3.25% and 3.58%, respectively. What makes this move structurally important is not the level…but the drivers:

- The immediate catalyst was political: cross-party talk of consumption tax relief, particularly food tax cuts, triggered a repricing of Japan’s fiscal path.

- At the same time, the BOJ has exited its old regime of yield suppression. The policy rate was lifted to 0.75% in December and long-end yields had already begun moving ahead of the hike.

- JGBs were the worst-performing G10 bonds in 2025 driven by sustained BOJ tightening and rising fiscal uncertainty; the long-end forward yields of the curve are now comparable to US Treasuries.

- Critically, this is occurring as Japan’s structural buyer base changes. Domestic life insurers have historically been the natural absorbers of long-dated JGB supply. Now, they have become net sellers, leaving foreigners as the marginal price setters. This is unchartered territory for Japanese markets.

- That alone makes yields more sensitive to fiscal headlines, FX volatility and global risk sentiment.

- Japan is no longer a “policy-protected” bond market. It is being priced like Italy – not Switzerland.

With Japanese inflation now hovering around its target levels, markets are moving away from the old practices (i.e. “liquidity-trap dynamics) that resulted in a weakening of the Yen when inflation rose and also flattened real rates. Instead, the combination of fiscal expansion (see below re political landscape) and gradual BoJ rate tightening results in a weaker currency. In turn, this leads to higher long-end yields and a steeper curve. It’s the reason financials did so well last year.

This phenomenon can only reverse if future policy is able to restrain fiscal spending and/or tighten monetary policy even further. What distinguishes this episode from previous reflation phases is that politics, not inflation, is now the dominant driver of the term premium (extra risk compensation sought) because nearly all major parties have embraced some form of consumption tax relief heading into the upcoming, snap election on 8th February.

The problem is not tax cuts per se but the lack of credible funding. Japan already carries public debt equivalent to roughly 230% of GDP – the worst ratio in the G7. Investors are no longer prepared to assume Japan can permanently expand fiscal space without consequences. This shift is visible in:

- The persistent rise in risk premia (extra return demanded by buyers) at the long-end of the curve.

- Heightened sensitivity of yields to political rhetoric.

- The increasing correlation between yen weakness and bond selloffs.

Organisations have tried to calm the market e.g. S&P’s sovereign team have argued rising tax revenues have kept the interest burden manageable. However, this reassurance is conditional: if we experience prolonged Yen depreciation and/or a visible erosion in GDP (growth), credibility will very quickly result in a revision of their assessment. Japan’s bond market has moved from being isolated/insular to one where the bond market is now disciplining fiscal behaviour in real time…something it has not done for decades! This repricing is occurring against the backdrop of a materially altered political landscape.

What has changed in this political rejigging?

- Coalition realignment on the right: The long-standing LDP–Komeito partnership is over. PM Takaichi now governs with the Japan Innovation Party (JIP), a reformist, libertarian-leaning group.

- The centrist opposition bloc has consolidated: In response, the Constitutional Democratic Party and Komeito (previously LDP’s partner) have formed a new Centrist Reform Alliance (CRA) that explicitly positions themselves against Takaichi’s rightward tilt and fiscal activism.

- Policy fragmentation and populist drift: Instead of a clean fiscal-vs-growth debate, Japan has drifted into a multi-party contest over “who cuts taxes more convincingly” and echoes populist dynamics seen elsewhere in the world.

How do the parties differ?

LDP (Takaichi) + JIP (Japan Innovation Party): PM Takaichi has framed the election as a personal referendum and openly argues for ending “excessive austerity” and underinvestment. Markets interpret this as:

- Pro-growth (at least by intention)

- But fiscally tolerant in its execution i.e. a bit loose with the purse strings

- With the risk that campaigning priorities (i.e. say anything to woo voters) dominate over fiscal discipline.

- LDP: wants proactive investment in 17 strategic fields (e.g. AI, semiconductors, quantum & fusion energy).

- LDP: accelerate discussion on cutting consumption tax on food to 0% for two years.

- LDP: Establish rules on land acquisitions and ownership registration for foreigners.

- LDP: Relax restrictions on defence exports.

- LDP: legislate to establish an entity that reviews foreign investments in Japan.

Centrist Reform Alliance (CDP + Komeito): The CRA has made fiscal credibility its differentiator by:

- Advocating tax cuts only alongside targeted funding

- While rejecting the continual issuance of bonds for managing deficits as a financing tool

- Criticising Takaichi’s policies as undermining confidence in Japan’s finances.

- Eliminate consumption tax on food permanently, starting autumn 2026.

- Establish a SWF to create new, national revenue.

- Adhere to non-nuclear weapons principles in line with “spirit” of Japan’s pacifist constitution.

- Give assistance to home renters, reduce social insurance payments for lower-income people.

- Change the law requiring a single surname for married couples.

What do opinion polls say?

Japan has a semi-proportional mixed electoral system with general elections taking place every four years. Just over 60% of members (= 289 seats) are elected via a single-seat (first-past-the-post) system (like here in the UK) while the remainder (= 176 seats) through PR (Proportional Representation). The latter sees the country divided into 11 regional blocs, each returning between 6 and 30 members.

Opinion polls by two media outlets have the LDP in front – especially in districts with many conservative voters. One is a Nikkei survey which has the LDP on course to win 243 seats (more than the 198 seats on 23rd January when the Lower House was dissolved). 233 is the threshold needed to for a majority (total seats: 465). If achieved, it would give the LDP a stable, working majority, enough to chair all standing committees and allow operations to run smoothly.

The LDP leads in nearly 40% of the 289 single-seat districts nationwide. It dominates in the Yamaguchi, Tokushima and Kimamoto prefectures. However, in over 150 districts, the race remains tight as the LDP faces strong competition from other parties. The CRA is projected to win less than 100 seats (it had 167 seats before the Lower House was dissolved). Together with the JIP, an LDP-JIP coalition is set to secure 261 seats.

Another poll (by Yomiuri Shimbun) indicated the LDP is likely to secure a standalone majority with particularly strong leads in the Chugoku and Kyushu regions. It even thinks it could sweep all seats in Toyama and Tottori where both have strong conservative bases. The JIP is holding firm in Osaka – but is struggling in the PR vote.

In summary: The key question on 8th February is “does the result reduce or entrench fiscal risk premia?” Three outcomes matter most:

- Strong LDP–JIP mandate: Markets will tolerate higher yields – but volatility will only ease if the fiscal rhetoric (i.e. spend, spend, spend) moderates post-election.

- Weak LDP victory / fragmented parliament: This is the highest volatility outcome – it will result in policy drift, prolonged budget negotiations and persistent term premium. This would be the worst outcome.

- CRA-led or CRA-influenced coalition: This will likely be bond-positive initially (signalling fiscal consolidation to the market) but then growth expectations will be scrutinised and most likely challenged. After that, who knows!

MARKET SUMMARY...

- Another strong week for the commodity complex – despite a technical correction to gold and silver over Trump’s mixed messaging around the US$.

- Trump has nominated Kevin Warsh as Powell’s replacement for Fed Chair. His confirmation is not in the bag: it has to be approved by a Senate Committee – and one Senator, Thom Tillis (R) has indicated he will block any Fed nominee until the Justice Dept probe into Powell is completed. However, Warsh’ credentials are not in dispute. The announcement saw the US$ pare gains and the Treasury yield curve steepen (i.e. yields rose/bonds prices fell) as Warsh is seen as quite a hawkish choice – unusual seeing as Trump has been lambasting Powell for not easing rates aggressively. Markets do not expect much action as they price in two more rate cuts this year. This would take the benchmark down to around 3% (some call this the “neutral” rate).

- Oil (WTI) has run to the mid-$60s on the back of rising Gulf tensions. The longer it stays at these and higher levels, the greater to inflation – which is already sticky and outside the Fed’s range.

- FX volatility has left many concerned, especially recent US$ weakness spurred by Trump’s comments that implied he’s comfortable with the US$ at these levels. He seems to be weaponising it – weaker US$ is not great for foreign exporters to the US. The US$ has traded down on the week. These moves are political – not fundamentals. Data releases are US$ supportive so far.