Last week I outlined some key factors that will shape 2026. The biggest, by far, will be the continuing saga around AI and its impact on the economy, politics, defence…right down to the cost of living! The sheer levels of capital that have already been deployed – and the amount still to be deployed – is mind boggling. Perhaps the best way to look at this is to ask what the adoption rate has been so far at firm level (various sources shown to the right):

| Metric | Definition | 2025 (Current) | 2026–27 (Projected) | Notes / Source |

| Firm-Level Adoption (Global) | % of firms using at least one AI tool or capability | 17–22% | 30–35% | McKinsey AI Survey, BCG, PwC Barometer |

| Firm-Level Adoption (US) | US firms reporting operational use of AI | 25–30% | 40–45% | PwC (US-focused), MIT Sloan |

| AI Usage Penetration (within firms) | % of functions / business units in adopter firms where AI is deployed | ~45% | ~70–80% | McKinsey, DB, GS – shift from isolated to enterprise-wide deployment |

| AI Deployment Maturity | % of firms using multiple AI use cases at scale | 11% (Global) | 25–30% | BCG June 2025 report – “Mature adopters” |

| SME Adoption | Small & medium firms using AI | <10% (Global) | ~20% | Adoption remains low; infrastructure/cost barriers remain |

| Top-Quartile Sector Adoption | Leading sectors (Tech, Financials, Telcos, Healthcare) | 40–50%+ | 65–75% | BCG, McKinsey; especially high in Customer Ops, Marketing, R&D |

| Manufacturing / Industrial | AI adoption in factory ops, supply chains, robotics | 15–20% | 30–35% | McKinsey Ops report; slower due to Capex/hardware requirements |

| AI Adoption in Emerging Markets | Non-OECD countries’ firm-level AI usage | <10% | ~20% | PwC & GS reports – lagging digital infra, skills & access |

From the above, adoption is growing but is still low in absolute terms. Furthermore, more than 2X growth is expected in firm-level adoption by 2026 globally. Importantly, the bigger shift is in the depth of usage within companies across functions (regardless of whether it is AI or non-AI related). While the uptake is high in tech-heavy industries, EM lags. What then are the implications for chip demand (AI and non-AI related)? See table below:

| Chip Category | Outlook | Commentary |

| AI Accelerators (GPU/ASIC) | Very strong growth | Driven by model training, inference at scale, LLMs, vision and audio tasks |

| Data Centre CPUs | Strong growth | Necessary to support AI pipeline and orchestration around accelerators |

| DRAM / HBM (High-Bandwidth Memory) | Strong growth | AI models need vast memory access speeds; HBM3 in huge demand |

| SSD / NAND Flash | Strong growth | For storing model parameters, intermediate outputs, training data |

| Networking Chips (NICs, switches) | Strong growth | Needed to handle massive I/O in multi-GPU setups and distributed computing |

| Edge AI Chips (e.g. for robotics, IoT) | Niche but rising | In industrial/manufacturing deployments |

| Power Management / Cooling / Specialized Logic | Indirect growth | Thermal, energy-efficient components become critical to manage high power use |

The above implies 2026/27 will be a very capacity-constrained year for AI Chip suppliers (Nvidia, AMD, Intel and TSMC are all racing to ramp up capacity; the Hyperscalers (AWS, Microsoft, Google Cloud, Meta) are designing custom silicon (application-specific integrated circuits or ASICs, engineered to perform a single type of task extremely efficiently rather than being general-purpose CPUs) to reduce dependency and costs (e.g. Amazon Trainium, Google TPU). The impact of all this is to drive a boom in non-AI Chips (especially for general-purpose server chips, networking & memory).

This brings me on to the AI-Power Infrastructure situation i.e. the power supply – both existing and required – to facilitate the above growth rates! The table below summarises the complexity behind this using various sources

| Topic | Summary | Supporting Comments from Reports |

| Current Global Data Centre Power Usage | 415-460 TWh per year (this is 1.5% to 3% of global electricity); AI workloads consumes 5% to 15% of that consumption. | [Goldman Sachs (Dec 2025)]: The present grid is capable of powering current AI/Digital infrastructure because AI is a small slice of broader electricity use. This is rapidly changing! |

| Forecast AI-Driven Power Demand (by 2030) | Doubles to 945 TWh/year; in extreme growth case, could reach 2,000 TWh by 2035. AI-driven workloads may account for 35% to 50% of data centre use. | DB (Nov 2025) & GS (Dec 2025): Global electricity demand is currently growing at 3% to 4% pa. AI data centre power needs are increasing 2–3× faster than the current growth rate! Implies a 10% to 15% CAGR in power demand from AI alone. |

| Growth Required in Power Grid Capacity (2030 target) | +110% growth (compound) vs 2023 levels. | McKinsey & PGIM: Growth in demand far outpaces infrastructure expansion; grid needs to double output in 5–7 years to keep pace. |

| Actual Grid Expansion Rate (Current CAGR) | About 2.4% globally (4% in China, under 2% in US/EU); this could call for over $3tn spend by 2028 to support AI expansion. | PGIM (2025) & GS: Major lag in developed markets; permitting delays, NIMBY (Not-In-My-Back-Yard) constraints, lack of transmission investment cited. |

| Gap Between Required and Actual Grid Growth | Shortfall of about 7–10% CAGR | GS & PGIM: Grid investments globally are some $300bn/year vs the required $600bn/year; this is a serious mismatch and overlooks the time required to roll it out (2y to 5y+). Grid growth is steady and incremental; AI demand is lumpy, concentrated & accelerating. Some regions (e.g. EMEA) are already experiencing power constraints and are already trying to slow data centre buildout. |

| Estimated Infrastructure Cost to Close Gap (2024–2030) | $2.5–3.0 trillion globally! | DB & GS (2025): Includes renewables, HVDC lines, grid-scale batteries; assumes US and China drive bulk of CAPEX. |

| Timeline to Close Infrastructure Gap | 7–10 years (realistically)[Compares current total electricity growth of 3%-4% vs the 8%-12% needed to meet AI growth alone] | DB: Even with accelerated approvals and funding, grid builds take time. High voltage lines often require 5–7 years from planning to operation. |

| Feasibility of Achieving Power Targets | Partially achievable but requires policy acceleration and private capital (more achievable in China vs elsewhere due to all sorts of regulatory, environmental and consumer challenges). | PGIM & BCG: Realistic only if (i) AI datacentre efficiency improves, (ii) power-hungry models shift to edge/low-power inferencing, (iii) governments streamline energy permitting. |

Given all the above, what then is the likely impact of AI on Power growth required, the AI adoption acceleration, EPS (Earnings Per Share) growth impact, Valuation impact vs today, Productivity impact, the Uplift to GDP and the Inflation impact? The table below (the last I promise!) summarises it:

| Scenario / | Power Growth | AI Adoption | EPS Growth Impact | Valuation Upside | Productivity Impact | GDP Uplift | |

| Year | Assumption (CAGR) | Acceleration | (Annualised) | (vs Today) | (Average p.a.) | (By 2028) | Inflation Effect |

| Consol. Best Case | +15% (Aggressive Buildout) | Rapid (50–60%+ by 2028) | +5.0% | +45–65% | +1.5–2.0pp | +6–8% | Mildly Disinflationary |

| Consol. Base Case | +8% (Steady Investment) | Moderate (30–40% by 2028) | +2.5% | +20–30% | +0.8–1.0pp | +3–4% | Neutral to Mildly Disinflationary |

| Consol. Worst Case | +3% (Grid Bottlenecks) | Slow (20–25% by 2028) | +0.8% | +0–10% | +0.3–0.5pp | +1–2% | Neutral to Sticky |

| 2026 Best Case | +15% (Aggressive Buildout) | Rapid (50–60%+ by 2028) | +5.0% | +15–20% | +1.5–2.0pp | +2% | Mildly Disinflationary |

| 2027 Best Case | +15% (Aggressive Buildout) | Rapid (50–60%+ by 2028) | +5.0% | +15–20% | +1.5–2.0pp | +2% | Mildly Disinflationary |

| 2028 Best Case | +15% (Aggressive Buildout) | Rapid (50–60%+ by 2028) | +5.0% | +15–25% | +1.5–2.0pp | +2% | Mildly Disinflationary |

| 2026 Base Case | +8% (Steady Investment) | Moderate (30–40% by 2028) | +2.5% | +5–10% | +0.8–1.0pp | +1% | Neutral to Mildly Disinflationary |

| 2027 Base Case | +8% (Steady Investment) | Moderate (30–40% by 2028) | +2.5% | +5–10% | +0.8–1.0pp | +1% | Neutral to Mildly Disinflationary |

| 2028 Base Case | +8% (Steady Investment) | Moderate (30–40% by 2028) | +2.5% | +10–15% | +0.8–1.0pp | +1% | Neutral to Mildly Disinflationary |

| 2026 Worst Case | +3% (Grid Bottlenecks) | Slow (20–25% by 2028) | +0.8% | +0–3% | +0.3–0.5pp | +0.5% | Neutral to Sticky |

| 2027 Worst Case | +3% (Grid Bottlenecks) | Slow (20–25% by 2028) | +0.8% | +0–3% | +0.3–0.5pp | +0.5% | Neutral to Sticky |

| 2028 Worst Case | +3% (Grid Bottlenecks) | Slow (20–25% by 2028) | +0.8% | +0–5% | +0.3–0.5pp | +0.5% | Neutral to Sticky |

To wrap up:

- The trajectory of the AI-driven economic impact, over the next three years, will hinge critically on the pace of power grid expansion as well as the rate of adoption.

- As shown, a best-case scenario gives a huge uplift in EPS (5.0% pa) with valuation multiples expanding as much as 65%. The boost to GDP is huge (6% to 8%) and, vitally, the impact on inflation is mild at worst. Most likely, because of the boost to productivity, it will be disinflationary.

- However, even the worst-case scenario is not that bad assuming power grid bottlenecks AND slow(er) adoption rates. It does mean more tempered valuation increases – and if these are perceived by markets as ominous, then we will see volatility as the proverbial bears advocating a “dot.com part II” collapse will come back in force.

- From here, policymakers and investors have to grapple with whether they think real-world capacity can keep pace with AI’s ability to deliver something exceptional.

- From a portfolio construction perspective, one’s options are not solely limited to investing in Tech! While the latter should continue to remain a healthy portion of portfolio (depending on your risk appetite/tolerance/capacity for loss), there are other asset classes: These include energy infrastructure (given the above grid constraints and not forgetting the huge scientific advances being made to generate power in alternative ways); the latter comes with short-to-medium lending opportunities attracting double-digit rates (a great complement to equities and substitute for traditional fixed income); regional plays centred on expansion (e.g. less than 10% of EM firms use AI vs 25% to 30% in the US. This is a staggering gap but presents a dual opportunity to (A) invest in the roll-out and (B) arbitrage the leapfrogging! The proximity and network from China can easily accelerate this process from present levels). These are not exhaustive but certainly speak to some of the major themes.

- From the adoption rates shown across the tables above, what I am not seeing is a tapering – indeed decline – in take up. I see it continuing to spread across horizontal and vertical planes (existing markets while finding new ones). We are in a learning phase with AI – the more it improves, the greater the adoption.

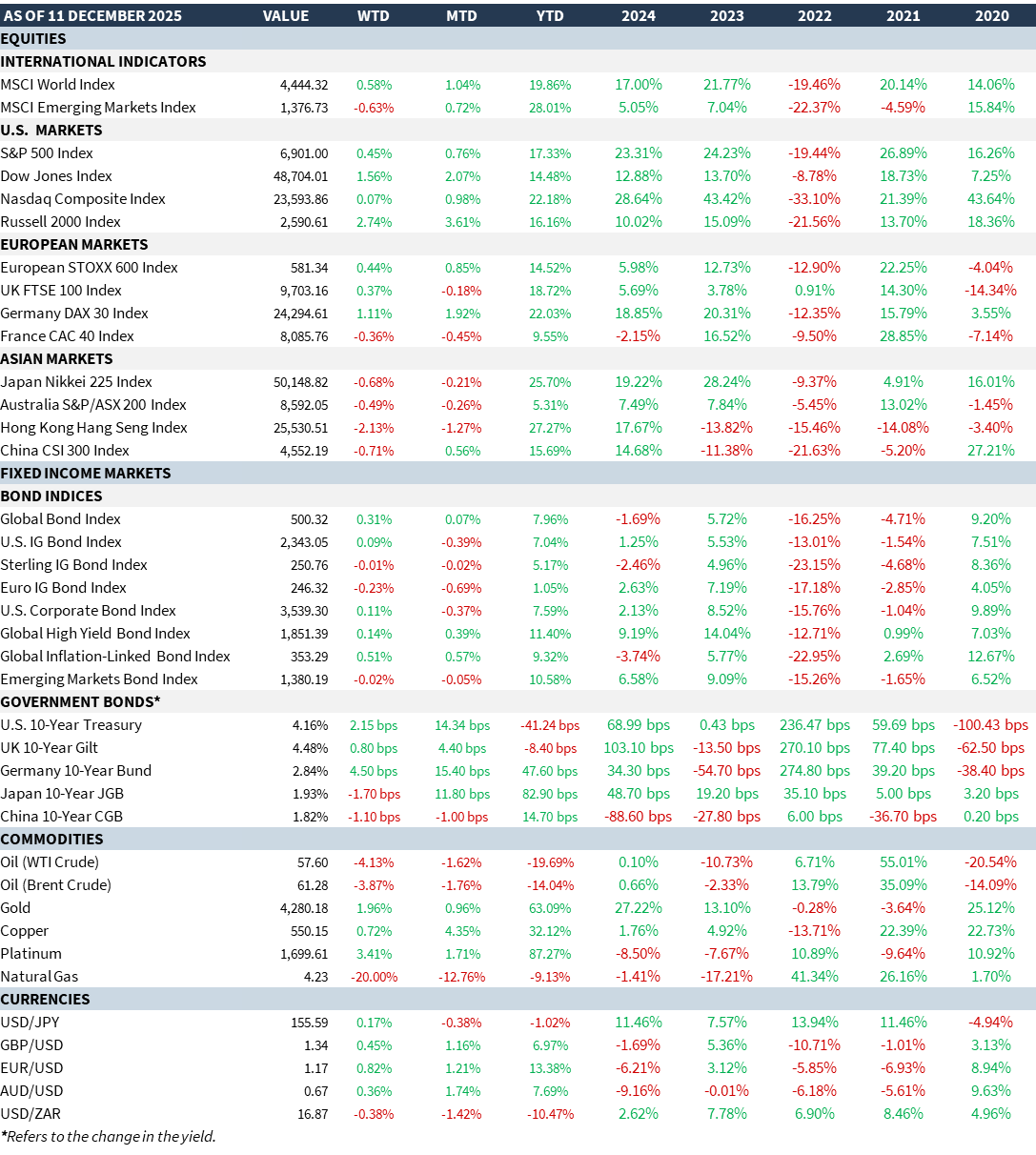

MARKET SUMMARY...