Update on Greenland: Following threats of force and implementation of further tariffs (from President Trump towards European NATO members), we seem to be heading towards a “framework” at Davos built largely around security. The issue of sovereignty was not on the table. By the sounds of it, there’s still plenty to discuss and so far European leaders only have an outline to go on. So what’s in Trump’s proposed framework over Greenland?

- Greater US/NATO security cooperation (so as to strengthen NATO’s role on both Arctic & High North security. Under discussion are provisions that would expand US access and ensure Arctic security. The latter effectively preserves and deepens US military presence. It would be a change to the 1951 Treaty to guarantee US military base requirements.

- Trump said he would include rights (or expanded roles) related to security infrastructure like missile defence systems (e.g. Golden Dome) and critical mineral access.

- He wants an “economic component” to be included in any deal and this includes mining rights.

- He wants measures to stop the Russians and Chinese from having any economic and military presence.

Regardless which direction these framework discussions evolve, one thing is certain however uncomfortable the truth appears: in today’s new world order (Cold War Part II), Europe collectively (not just Denmark) does not have the autonomous, military capacity to secure the Arctic, the North Atlantic or its own northern flank WITHOUT the United States. Bizarrely, this perceived softening in stance (what some have naively & foolishly labelled another TACO moment) tells us a lot about how Trump sees Europe: he does value it and their role in NATO (more for strategic reasons) but, at the same time, it’s an offer of continuity i.e. give us what we want and you get continued inclusion inside the US security architecture (US protection, NATO primacy, access to missile defences, etc.)………just that it will all be on revised terms. Key for him are (1) strategic alignment in Greenland and the Arctic, (2) reduced European veto in that region and (3) much-reduced opposition to US positioning. If Europe does not play ball, (most unlikely), then the US will no longer see them as an ally…….in which case, don’t be surprised by what the US does next! The US has too much invested in Europe to take a hard line with them.

Some points of interest from both sides’ perspectives:

- Polls suggest 85% of Greenlanders oppose being part of the US. If it ever came to it, I bet they would reconsider if the price was right!

- European leaders have recently described Trump’s approach as a form of neo-colonialism and warned of proportionate retaliation. The reference to “neo-colonialism” is somewhat ironic seeing as back in the day it was Europe invading other jurisdictions, especially the Americas (e.g. Spanish, Portuguese, French, Brits, Dutch). In fact, it was this that led to the “Monroe Doctrine” (1823) when President James Monroe stated the Western Hemisphere was closed to further European colonisation and intervention (referring to the Americas). In return, he pledged the US would not meddle in European affairs. Since then, President Trump coined the phrase the “Donroe Doctrine” – a similar attempt to exclude Chinese and Russian influence in the region (e.g. Panama, Venezuela).

- He spoke at length about how the US protected Greenland in WWII. He is correct – a “Defence of Greenland” agreement was signed between the Danish Ambassador and the US in Washington in 1941 following Denmark’s fall to the Nazis in a matter of hours! This defence was facilitated via a network of bases and troops. At the end of the war, administration of Greenland was returned to Denmark. US military presence diminished gradually over years. The US did try and buy Greenland in 1946 for $100mn in gold. At today’s prices, that would be worth $6bn. The Danes declined. There is an irony here similar to Panama that explains Americans angst. In both cases, they (the Americans) did the heavy-lifting and were left with nothing!

As for the estimated impact from the new tariffs (10% for now and then escalating to 25% end of Q1)? For the UK economy, it is some £4bn – this at a time when the UK can ill-afford further fiscal pressure. So how do you hedge? Geopolitics is no longer a uniformly bullish impulse for commodities. It is actually fragmenting across the commodity complex:

- There was a time when oil was a great hedge because it coincided with risks to the supply-side. Not anymore – it is colliding with amply supply, spare capacity and slowing marginal demand growth. For example, as a share of global GDP, oil used to be around 4.5% (early 2000s). Now it’s about half. Why? More capacity, more production efficiencies, more usage efficiencies, alternative energies and more caution around energy consumption.

- Meanwhile, metals are benefitting from supply tightness, electrification and strategic stockpiling. Energy transition, defence/re-armament, supply chain re-nationalisation and the China/West strategic competition – these are all boosting the case for metals.

Oil has lost its status as the default geopolitical hedge. Spikes in risk premia are transient – not sustained. Commodities are boosted only when supply is constrained – not from mere threats to demand. Commodities sit at the fault line of Goldilocks and Reflation. Goldilocks = growth + falling inflation; Reflation = growth + sticky inflation. For now, markets are leaning towards Goldilocks as growth is being upwardly revised while inflation optimism is still holding. Looking at specifics:

- Oil: an outright casualty of Goldilocks. Supply is plentiful – Venezuela now adds to that. If Iran implodes, new supply will come as part of incentive schemes. Even if it doesn’t, Iran’s capacity (some 5mbpd) can easily be absorbed. The recent events in Iran only moved risk premia slightly – before settling down again. No more hedge here!

- Gold: a true exception. It performs even in Goldilocks because it is not a growth input and hedges tail risks that markets are under-pricing.

- Copper: the long-term story is strong. It is however vulnerable to near-term growth disappointments. Therefore, you have to take a view on growth and the US$.

Gone are the days when geopolitics was generally assumed to be inflationary by default! Instead geopolitics:

- Redistributes pricing power. We are seeing this right now in the context of tariffs and the scramble to find new markets while the Venezuela episode has weakened the outlook for Canadian oil sands in favour of VZ.

- Favours strategic autonomy (defence, energy transition).

- Geopolitics no longer automatically lifts energy prices in the way it did back in the 1970s and early-2022.

The metals complex has clearly fractured. In the table below, I have tried to summarise some key drivers of sustainability and risks for this year:

| Metal | Category | Primary Price Drivers | What’s ACTUALLY happening |

|---|---|---|---|

| Gold | Precious | Geopolitical risk; Central Bank (CB) buying; Reserve diversification; tail risk hedging | Primary trading is no longer just about real rates or the US$; Instead, it’s about persistent official-sector demand from (especially EM CBs); continuing distrust over Fiat FX. |

| Silver | Precious/Hybrid | Spillover from Gold; industrial demand; speculative flows | Silver price behaves as a leveraged gold proxy – with cyclical volatility from cyclical demand; Drawdowns are far sharper. |

| Platinum | Precious/Industrial | Tight Supply and Auto | Supply constraints in South Africa supports prices but demand is uneven; structurally challenged by the EV transition. |

| Copper | Base | Energy transition, electrification, grid build-out, China demand | Long-term growth is intact; near-term growth setbacks cause pullbacks; sensitive to inventory rebuilds. |

| Nickel | Base | EV Batteries | Structural oversupply from Indonesia has overwhelmed demand optimism; Ni prices reflect supply-side shock – not demand growth. |

| Lithium | Energy Transition | EV adoption, Battery supply chains | Classic boom-bust; supply has ramped up faster than demand; despite its long-term relevance, its price reflects oversupply. Long-term relevance is still intact. |

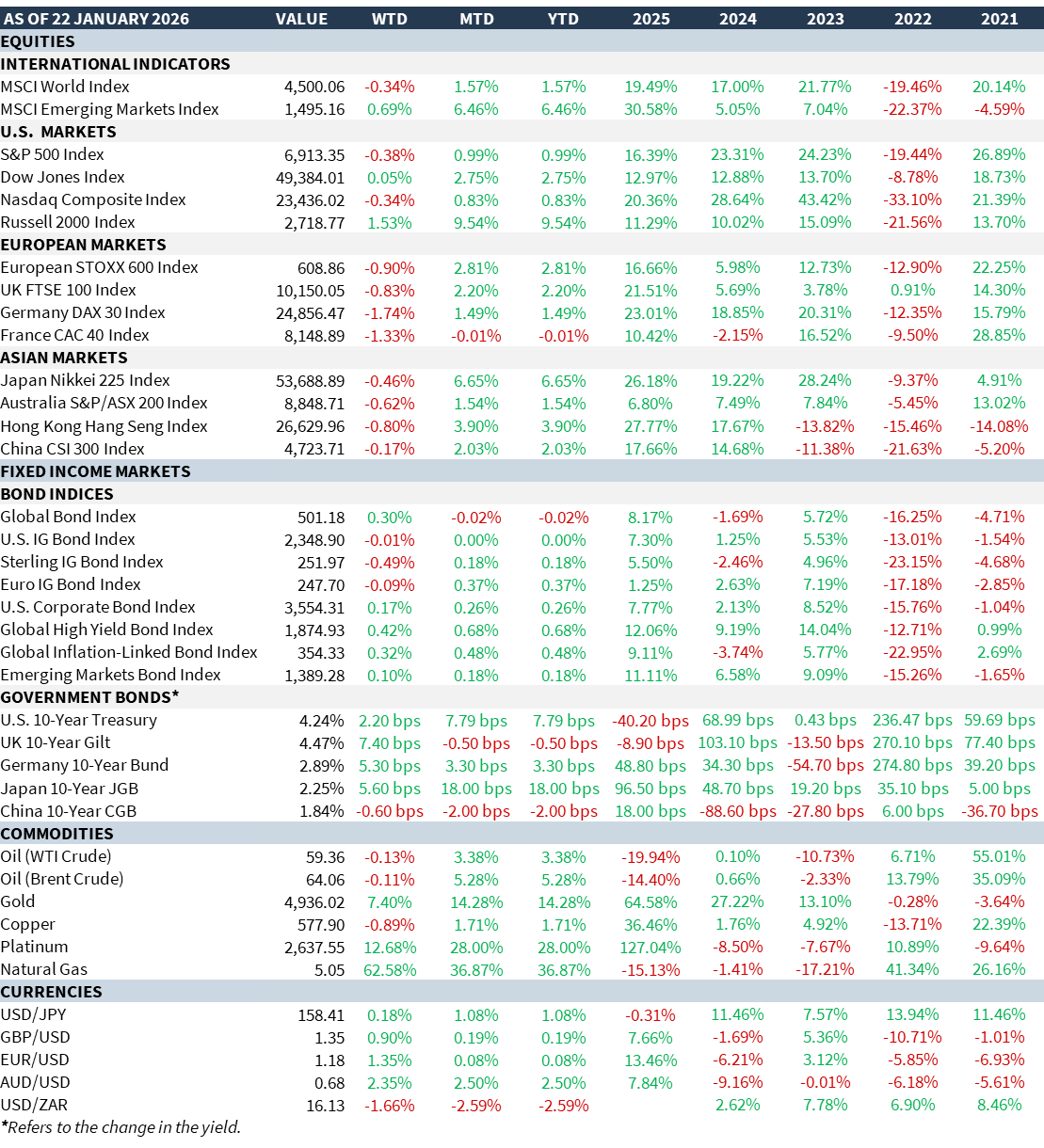

Market Summary...

- Global markets staged something of a recovery following Trump’s announcement he would allay the 10% tariffs depending on Greenland talks progress.

- Another spectacular run by Natural Resources and Precious Metals.

- US Q4 ’25 GDP was revised slightly higher – this will boost Base Metals.

- Japanese bond yields have endured significant volatility, especially as PM Takaichi calls a snap election on 8th Feb. Her party is calling for substantial fiscal easing – this led to yields on a 20y-bond auction jump to new highs (30y close to 4%). Arguably, long-dated yields are too high now.

- The week saw a sell-off in the US$ which has fallen over -1% on a Trade-weighted basis given recent events. With the Yen at close to 160 vs the US$, intervention is close.