We’re eight weeks into this conflict (start: 27th February). Iran does not need to close the Strait of Hormuz completely to disrupt shipping volumes. It just needs to make passage look unsafe. It is doing this through harassment & intimidation, seizure of commercial ships, imposing control mechanisms (e.g. charging tolls), tactical use of opening/closing the Strait, responding to the US blockade asymmetrically and maintaining ambiguity (e.g. ghosting). The net impact? 10 million bpd has been disrupted and oil has now settled between $100 to $110 pb! Look at the stats: pre-war, some 125 to 140 ships crossed per day; that number is down to less than 20 pd….recently, as low as 2 to 5 pd. It’s a near-choking of the Strait without a formal declaration of closure. If it were to cross this line, we would have a full-on resumption of bombing. Neither side – Iran more than the US – wants that. It’s trying to hang on to the remaining infrastructure it has.

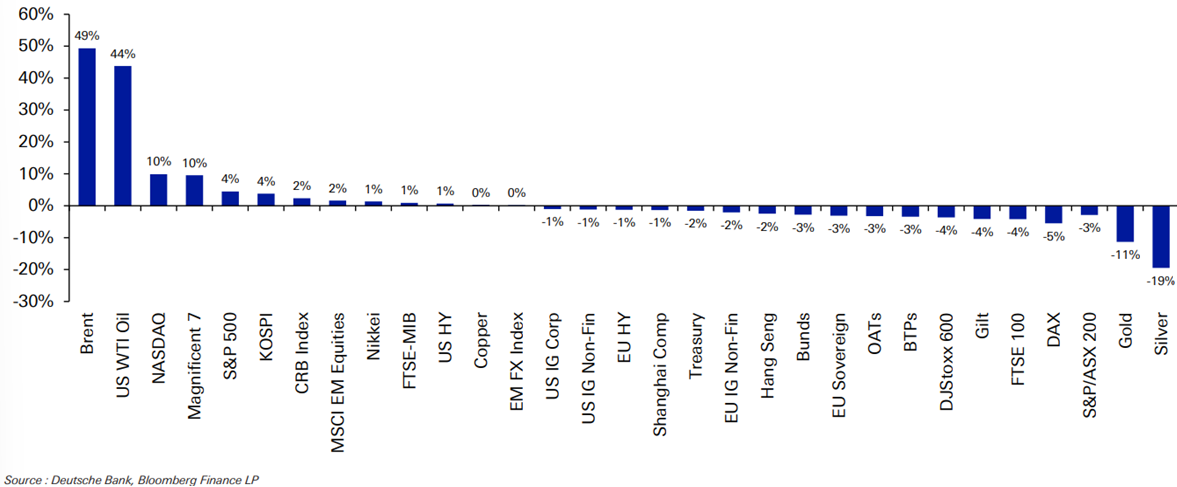

Total return performance of various financial assets, since the start of this war, is shown below:

- Brent is up +49% and investors remain of the view this will be temporary.

- US assets have outperformed. This speaks to the US being more insulated given its status as a net, energy exporter. The tech rally has boosted the S&P 500 and Nasdaq.

- South Korea (Kospi) is higher now than the start of the conflict. In local FX, it is up +58% YTD.

- EuroZone (EZ) assets are underperforming – they are exposed to the energy shock – like they were in 2022 just less so.

- Precious metals (gold and silver) have fallen. The US$ has remained resilient (see above point) and US$ reserve status has been boosted.

- Government Bonds have been hurt with yields rising globally. UK bonds have been the hardest hit (+74 bps).

Why are markets so sanguine? Basically, they think a deal will be struck – at least we get a lasting ceasefire. The problem is that neither side wants to give way! The IRGC seems to be in control otherwise we would be seeing unimpeded ship-crossings. Bear in mind 60% of Iran’s revenues come from oil and the objective here was to starve Iran of these valuable revenues. Yet, we do not seem to be anywhere near / close to that moment. Meanwhile, we are over 300m barrels short on supply (30 days x 10m bpd not getting through the Strait) while all this drags on. For context, March saw a supply deficit of 15mbpd and for April, this deficit has come down to 10 to 12mbpd. It looks like we will be stuck on 10 to 12mbpd – this translates into a total shortage of some 1.5b over Q2. This level of inventory draw is not sustainable (US Strategic Petroleum Reserves and China’s combined).

How does the UAE’s decision to leave OPEC change things? In the short-term, it doesn’t. In fact, the UAE’s announcement is well-timed given that oil prices are so elevated. The UAE wants “freedom to produce more oil, faster and on its own terms”, especially during a geopolitical shock. During the course of this war, it has suffered far heavier bombardment than any of the other Arab states. Its objective is to maximise revenue, reduce dependence on Saudi-led policy and be able to respond to conflicts more easily. Why now?

- Oil prices are elevated; demand outlook still strong; global supply still constrained. It does not want to be capped on its output when it can be taking advantage of economics.

- Frustration with OPEC – especially Saudi Arabia – for some time. It feels quotas are too restrictive and policy too slow. It wants to be nimble, agile.

- The Iran war has changed the equation (disruptions through Hormuz).

- Its exit weakens the OPEC cartel – helping it to align more with the US (Trump has long-criticised OPEC).

Significance?

- OPEC is weakening structurally. The UAE is its 3rd largest producer. OPEC will now find it harder to stabilise prices.

- The Gulf is fragmenting. Previously, it was Saudi + UAE; not anymore.

- The oil market will likely become more volatile as a result of a fading OPEC discipline (less coordination, more reactive production).

- Don’t expect any change in oil prices in the short-term while Hormuz disruption dominates. Thereafter, it starts to put downward pressure on oil as more independent producers come to market.

The UAE move also speaks to the changing relationship between Saudi and UAE, both of whom are big rivals in their quest to achieve dominance (financially & economically) in the region. The table below is a high-level summary of where they stand:

| Area | Relationship Status | What it Means in Practice |

| Scale | N/A | Saudi has the edge given its larger population, economy, territory and military depth. |

| Security / Defence | Aligned (Partners) | Joint interest in regional stability, containing Iran, avoiding full-scale war. |

| Oil Policy | Diverging (Rivals) | Saudi favours a controlled supply and remains the OPEC anchor; UAE wants flexibility and higher output. |

| Capital / Economic Hub | Competing (Rivals) | Riyadh vs Dubai/Abu Dhabi competing for global HQs, investment, talent. UAE has the edge though Saudi is closing the gap. |

| Regional Influence | Competing (Rivals) | Different approaches to power: Saudi geopolitical, UAE commercial/pragmatic. |

| Foreign Policy | Cooperation | Saudi puts security first; UAE is more pragmatic & commercial. UAE wins overall for its agility. |

| Israel | Somewhat Divergent | Saudi is cautious & conditional; tied to Palestinian/Arab legitimacy. UAE more open as evident in the Abraham Accords. |

| Iran | Mixed | Saudi wants containment but fears a full regional war; UAE seeks more hedging but is indirectly exposed due to its Israel ties/trade. |

| Overall Relationship | Competitive Partnership | Cooperation where necessary, competition where advantageous. |

The deeper, strategic difference is that Saudi thinks in terms of state power, longer-term control and geopolitical stability; UAE thinks in terms of commercial optimisation, flexibility and rapid response. Put simply, Saudi is a strategic controller; UAE is an opportunistic optimiser. So what does the future hold? It’s no secret the UAE has been toying with breaking away from OPEC for some time – it came close to doing so in 2022. The real answer comes down to whether Iran “wins” this war. In my opinion, it already has! This will determine who ends up dominant. In this regard, some thoughts on the scenarios are shown below:

| With Iran Intact (Base Case) | Without – or a Weakened – Iran | |

| Security order | Saudi continues to be the regional anchor for stability. | Less need for unified Gulf front. |

| Saudi strategy | Stabiliser role continues; cautious on escalation. | Reasserts leadership; faces less external constraint. |

| UAE strategy | Hedges bets: balances US & Israel; selective approach with Iran. | Acts more independently; expands influence. |

| Oil policy | Saudi pushes discipline via OPEC; UAE diverges. | Open competition on volumes. |

| Oil market impact | Geopolitics continues to dominate pricing. | Supply competition increases. |

| Israel dynamic | UAE deepens its ties; Saudi remains conditional. | Saudi more likely to normalise. |

| Iran factor | Remains a constant spoiler; limits rivalry among Gulf states. | Rivalry between Saudi & UAE intensifies. |

| Regional influence | Saudi leads formally; UAE builds networks. | Openly competitive. |

| Economic competition | Riyadh vs Dubai/Abu Dhabi intensifies. | Full-on competition for capital, HQs, talent. |

| Global alignment | Both aligned with US; UAE more flexible. | More bilateralism with US, China, India. |

| Market structure | Risk premium driven by Iran. | Pricing becomes supply-driven. |

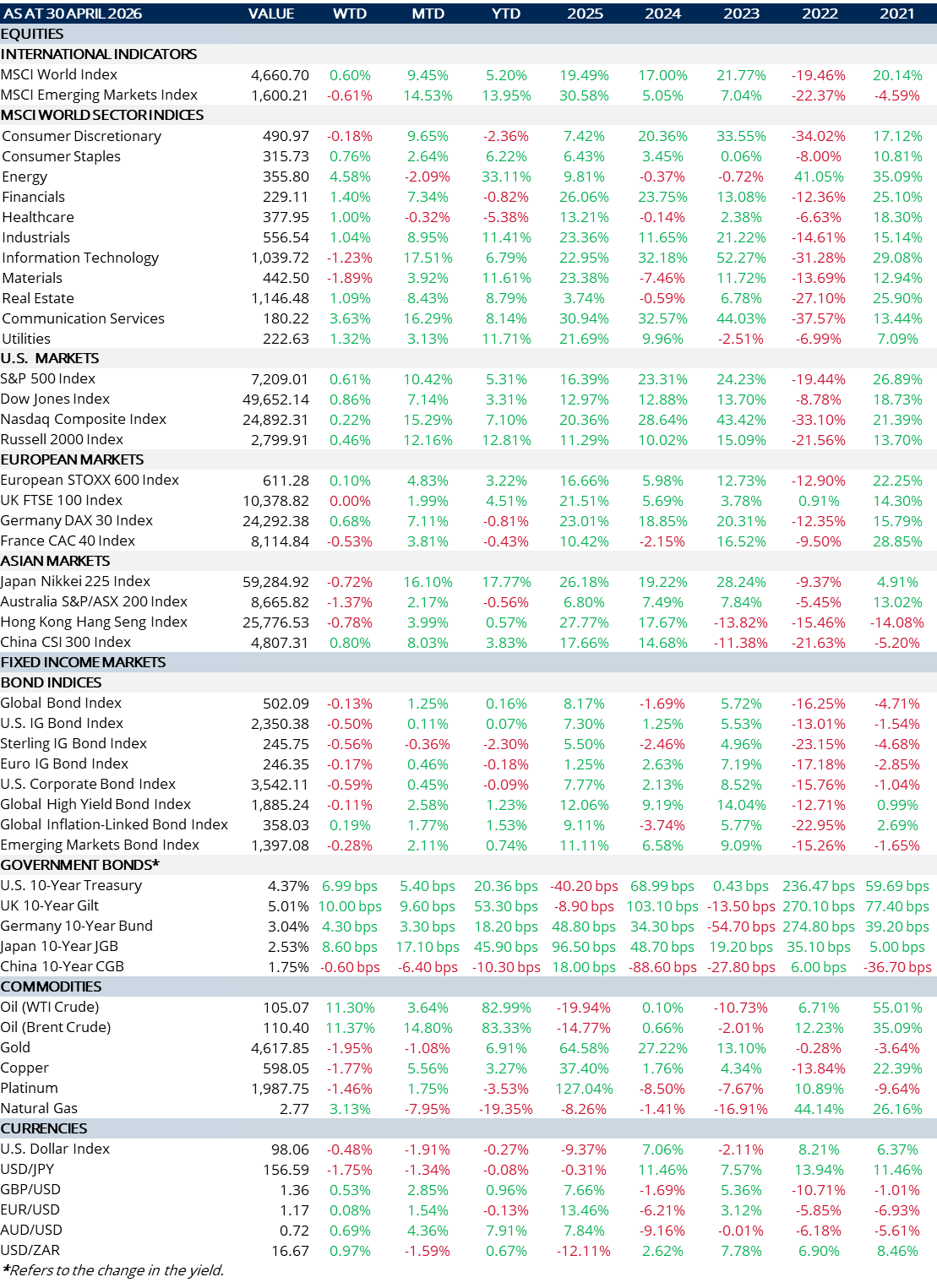

MARKET SUMMARY…

- Another month sails by. Equities still managed to clock up a positive performance on the week to close out a strong month

- ITC delivered a blockbuster +16.5% to +17.5% on the month! But there were strong performances all round registering +7 to +9%.

- YTD is also impressive albeit a little less so.

- In a classic “Risk-On” playbook, the US$ has slid almost -2%.

- Look where Oil is…..steadily rising….and yet there is continuing complacency around inflation. Meanwhile, bond yields (look at the 10y Gov. moves) are climbing higher. The UK 10y has even crossed 5%.

- Upcoming CPI (Inflation) prints are going to be so interesting. If markets end up being wrong-footed (as I suspect they will!), there will be massive “Risk-Off”.

- …..all said and done, I remain optimistic there will be a breakthrough in the US-Iran negotiations. I simply cannot believe stupidity will prevail!