It was a good weekend for PM Sanae Takaichi on all levels – personally and politically. She and her Liberal Democratic Party (LDP) achieved an outright majority in Sunday’s general election. Furthermore, her party’s coalition with the Japan Innovation Party (JIP) gave it a vital two-thirds “supermajority”. The chart below shows the revised standing of the parties in terms of seats.

Comparing “Before” and “Now”, the LDP’s share rose from 198 to 316 seats post-election, well above the 233 required for a majority! JIP went from 34 to 36 seats. The main opposition – the Centrist Reform Alliance (CRA) – crashed from 167 to 49 seats. LDP’s victory marks the largest in post-WWII history for any party.

Campaign issues & policies.

- Immigration. Some 40% of candidates – mostly from the ruling LDP/JIP Alliance – want to see changes in immigration policy to curb the inflow of foreign workers. This refers to both residents and visitors from overseas (the latter because of their concentrations in certain cities) resulting in cultural friction. It has also led to a surge in outsiders acquiring land and other real estate. Foreign workers totalled over 2.5mn as of end-October 2025, a +11.7% rise y/y and represent 3.7% of Japan’s total workforce (68mn). However, when asked what should be done, the picture becomes murky across party political lines. At one extreme, JIP was most adamant it wants to see curbs imposed on numbers allowed into the country. At the other, the CRA is heavily skewed to keeping numbers as they are, even accepting more! The LDP is somewhere inbetween. A finalised set of policies have been put together targeting foreigners covering Residency (language proficiency for permanent residency), Overtourism (right now tourists concentrate in certain locations – they wish to encourage them to visit other locations so as to ease the burden on local communities) and Real Estate (rules relating to nationality disclosure at time of acquisition).

- Fiscal policy/stimulus – near-term. Takaichi has promised a two-year freeze in the 8% consumption tax on food. This is aimed at helping low/mid-income households who have been struggling. It remains to be seen whether she goes through with this. Takaichi was not very engaging on this topic during the election – perhaps because of uncertainties around funding. She has made it clear she will reach out to the opposition to establish a “cross-party national council” with a view to compiling an interim report before the summer that will lay out the “basic framework of the cut”. She stated the two-year freeze would be paid for by “reviewing subsidies and special tax measures and tapping non-tax revenue”. The latter would be temporary until a proper system is put in place to automatically give a refundable tax credit. All this sounds like a combination of kicking the can down the road as well as some sort of dilution to the original idea of a freeze. In addition to freezing the consumption tax on food, other areas include transfers and subsidies for households, SMEs, energy and food costs. These are all aimed at supporting demand quickly in order to generate confidence & momentum. It is not structural change – the latter comes later to boost productivity (see “medium-term”).

- Fiscal policy/stimulus – medium-term. Stimulus will most likely pivot to (1) strategic CAPEX (semiconductors, AI/advanced manufacturing, energy security and defence industries) and then (2) supply-side growth support (incentives for private investment and aligning industrial policy with national security goals).

- Decision-making. With a two-thirds “supermajority”, the Alliance will be able to override any veto from the Upper House. It will even be able to initiate constitutional amendments. This should pave the way for a smoother and quicker policy-making process ahead unlike before. One such area will be over defence! Takaichi has signalled her intention to change Article 9 (“the pacifist/peace clause”) which renounces war and came into being in 1947. It was primarily written and imposed by the US. Ironically, the LDP – which was founded with the specific purpose of amending the constitution – has been unsuccessful in changing it (Article 9). Changing it is a two-step process: FIRST, a two-thirds majority is required in BOTH houses of parliament. Right now, she has just one – the lower house. In the upper, the LDP only holds 101 out of 248 – and no election is due for the upper house until 2028. The SECOND requires a national referendum. This process has never been tested. Timing is everything. She will need to prove herself to the public first and then, come 2028, have successful elections for the upper house and then go to the country!

Implications of the above.

- Markets: The immediate reaction was a further decline in the Yen (=higher fiscal deficit on the back of a planned freeze in the consumption tax on food and other items), a rise in longer-dated bond yields and a jump in equities. These moves reflect a dovish stance around fiscal policy and tolerance towards the normalisation of monetary policy.

- Looking ahead, economists are expecting higher rates. Goldman’s base case is for a hike in July this year (April or June also plausible). They also expect the terminal rate to reach c1.5% describing this as neutral. In essence, they no longer see Japan as an outlier compared to previous years or decades. Rate policy has now morphed into a more conventional hiking cycle. Three key indicators will be carefully watched: the March Tankan survey (focused on corporate profits and CAPEX), the April CPI print and SME wage data. Any one of these could prove to be the trigger for further yen weakness and therefore higher imported inflation. Goldman Sachs identifies a USD/JPY rate at or above 160 as materially raising the probability of earlier tightening. Any FX intervention by the BoJ will only be effective if paired with rate hikes.

- As for the yield curve, the ongoing rise in the 10-year and 30-year JGB yields is being tolerated for now. The days of near-zero yield volatility are gone — volatility is now a consistent feature of policy rather than something to be suppressed. This approach is aimed at restoring price stability rather than enforcing yield caps. If successful, it should raise policy credibility, echoing Takaichi’s pre-election rhetoric that “monetary policy is the BoJ’s responsibility.” If it backfires, inflation will persist and the yen will weaken further, forcing additional rate hikes and risking a destabilising downward spiral — an outcome that would be catastrophic.

Internationally, things become interesting:

- China: Tensions have been rising of late. China would have preferred a weakened Takaichi – instead, the supermajority does the opposite. Over the last twelve months, China has taken a tough/coercive stance with Japan by applying rare-earth export controls, economic pressure and a diplomatic freeze in the hope it would apply political pressure domestically and force moderation. Instead, Japanese voters have rejected this coercion while raising the prospects of amending Article 9.

- US: Takaichi’s emphasis on defence reform, economic security and strengthening resilience over supply chains will be welcomed by the US who has always wanted allies to carry more responsibility over regional security. This is fine – so long as Japan and the US maintain an alignment of interest – especially over Taiwan, containing China risk and an investment framework. On the latter, the US is becoming increasingly frustrated the $550bn pledged by Japan (following tariff talks) has yet to materialise! The relationship between the two – as is so typical under Trump in its dealings with other countries – is becoming much more transactional. That puts Japan in a precarious situation: it places constraints on how Japan goes about pursuing its own economic policies. Trump can’t handle bureaucracy – it impedes his leverage.

- South Korea: across Asia, regional democracies are finding they have to cooperate given that US attention is not what it used to be. With its new-found majority, Japan can pursue a new line in relations that not only helps forge a strategic tie between the two but also the trilateral (US-Japan-SK) cooperation.

- Others: the road ahead is now paved for Japan to freely seek/revitalise relations with India, Vietnam and Philippines in a way previously weak and fragmented Japanese governments could not.

This election allows Japan to choose sides and play a decisive role in the region. It can offer itself as a new partner – rather than constantly hedging its bets. Both China and the US will need to revamp their approach towards Japan as the latter becomes more autonomous. The clearest beneficiaries appear to be defence, aerospace, energy (nuclear & grids), semiconductors, advanced manufacturing, construction and general infrastructure. A supermajority is a big boost for anything defence-related (e.g. shipbuilders) and especially to restart anything nuclear.

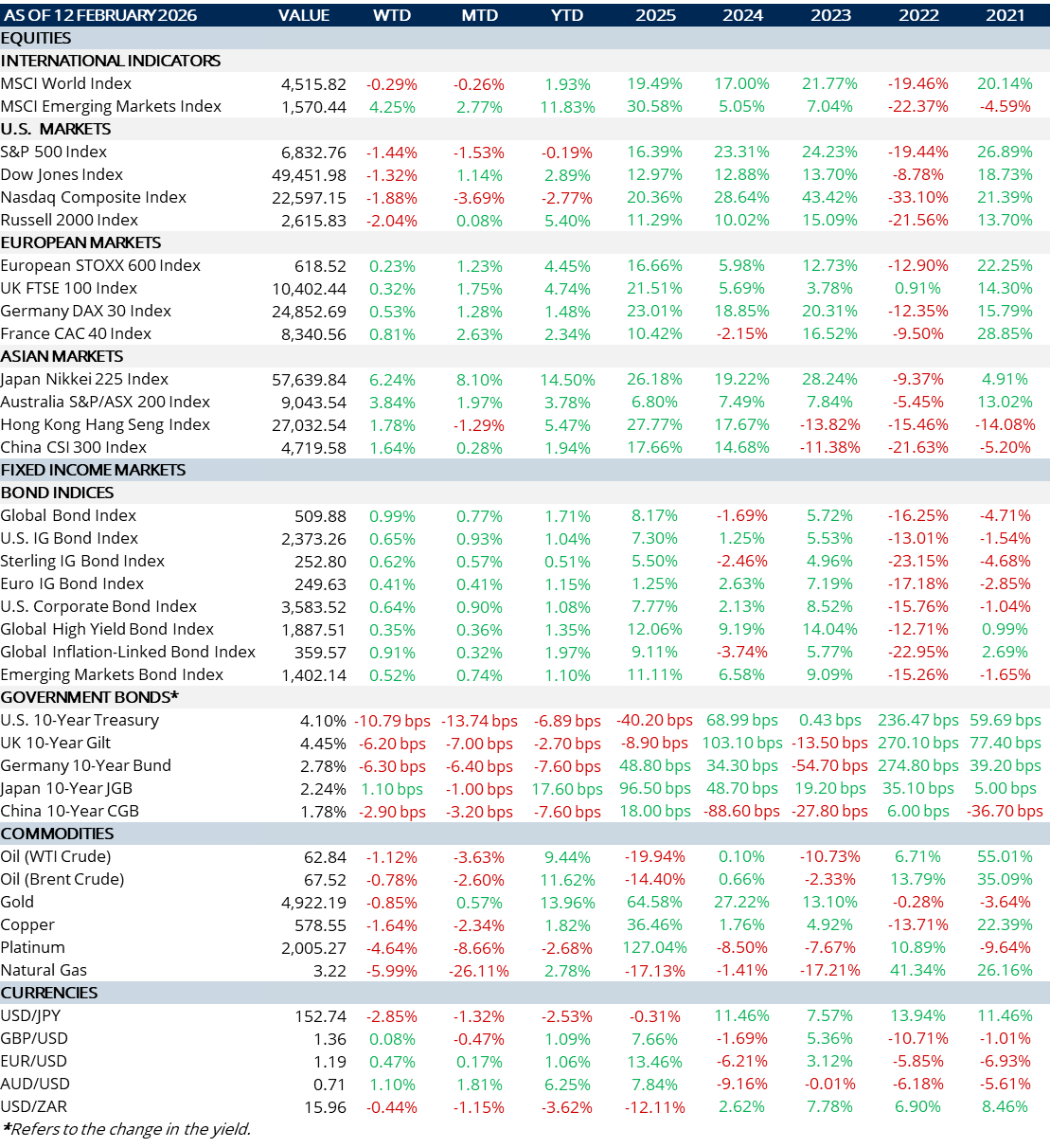

MARKET SUMMARY...

- A good week for equities in Japan following the election outcome (see above analysis).

- US Treasury yields have hovered mostly sideways. We had a good January payrolls number but US equities have drifted downwards with a continuing tech sell off (despite a stable environment and more capex upward revisions) and rotation into other sectors. Alphabet placed $20bn of debt into the market – an issuance that included 100y bonds! As one report said, only 25 years ago it had its roots in a garage! Today’s Headline CPI (Inflation) print was lower than expected (+0.2% m/m; +2.4% y/y) while Core CPI was as expected (+0.3% m/m; +2.5% y/y).

- The ongoing political crisis in the UK saw more, key resignations. The Epstein connections seem to be running deeper and wider than initially thought. The main worry for financial markets is an even further move to the left. The likelihood is that GB£ will start to come under downward pressure.