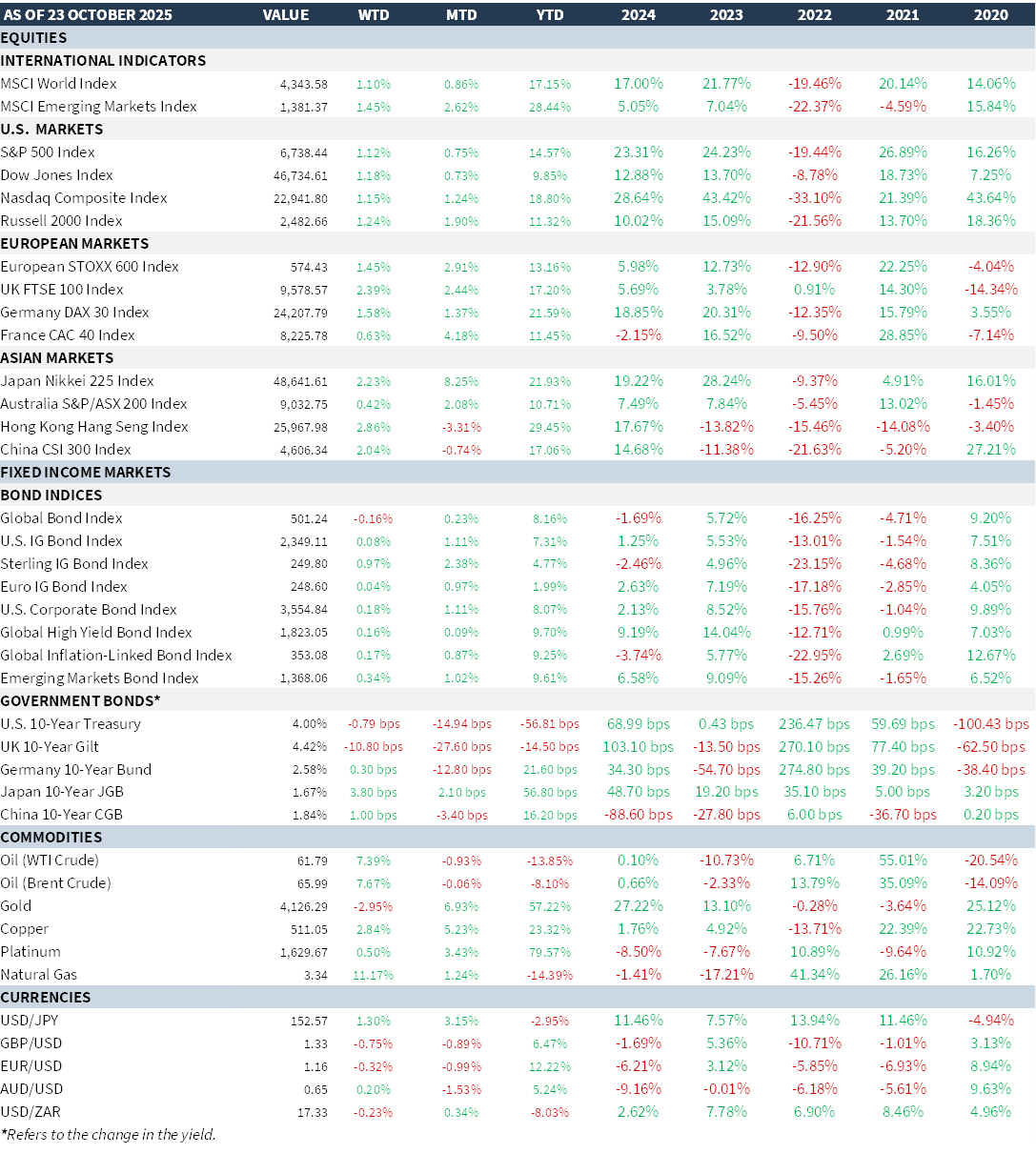

Gold has had an extraordinary rally in recent months reaching a peak of $4,359 per oz on 20th Oct. Markets – like they always do because too much of a good thing seems to scare people – saw the coming together of a number of factors that then dragged it down to $4,065 on 22nd Oct. Since then, it has risen and currently (mid-morning, today) the spot price stands at around $4,072 per oz. The gold price had rallied for nine, straight weeks – something that has happened only five times in history. Each previous streak ended with a major pullback averaging -13% in the ensuing, 2 months. Look at the table below summarising price action on some previous, notable occasions:

| Cycle | Rise % to Peak | Peak | Drop % | Time to Collapse | Main Trigger |

| 1979–80 | +390 % (from ~$185 in 1976 → ~$850 in Jan 1980) | $850 | −65 % | ~1 year | Volcker rate shock + USD rebound |

| 2011 | +170 % (from ~$700 in 2008 → ~$1,900 in Sep 2011) | $1,900 | −45 % | ~2 years | QE taper + rising real yields |

| 2020 | +75 % (from ~$1,270 in Aug 2018 → ~$2,070 in Aug 2020) | $2,070 | −15 % | ~6 months | Vaccine reopening + yield rebound |

| Current

2025 cycle |

+94 % (from ~$2,100 in Mar 2025 → ~$4,072 in Oct 2025)** | $4,072 (so far)** | — | — | Real-yield collapse, central-bank buying, fiscal-debt stress, and global hedge flows |

One of the key drivers for the rise in the gold price has been unprecedented fiscal deficits and record official-sector (Central Bank) buying. We have exactly the same thing today! And two, key risk triggers for its reversal are (1) a sharp rise in real yields and/or (2) a resurgence in the US$ – provided markets feel confident about pricing in tighter, fiscal discipline or higher policy rates (better carry returns for investors seeing as gold pays zero coupon).

The confluence of factors that resulted in the most recent spot price correction were:

- Investor trepidation that inevitably forces profit-taking when there’s too much of a good thing.

- Some positive developments that had formed around US-China trade talks. Note, this then reversed when China “unexpectedly” retaliated by suspending rare-earth exports, quickly catching the US off-guard.

- A strengthening of the US$: remember the US$ and commodities share a natural, inverse relationship and the US$ – which has declined since the start of this year – saw short-covering (i.e. the buying back of US$ shorts) leading to a rise in the US$ and therefore a natural fall in commodity prices (Gold being one of them).

- Overstretched technicals impacting traders (CTA’s, Algos, Systematics, etc.).

- Uncertainty on investor positioning due to the US government shutdown.

- The seasonal buying spree coming to an end in India (Diwali holidays).

The irony is that the long-term story for Gold has hardly changed:

- Inflation remains sticky.

- Government spending is becoming so out-of-control, it is seriously jeopardising the monetary system. US debt has crossed $38tn for the first time ever having risen $400bn in a single month!

- Faith in the US$ is being questioned.

- Central Banks continue to buy and hoard (see further breakdown below).

- Rate-cutting has begun and the debate is centred over how aggressive it will be.

- Geo-politics – driven by Russia/Ukraine – is far from over; in fact, following recent actions with President Trump forcing sanctions on Russian oil companies, it is set to elevate.

- Oil price movements benefit Gold both ways – the more they decline, the more pressure to cut rates and the higher they go, the greater the instability and knock to the financial system.

- Possibly more losses to come from US Regional banks.

Markets rarely move in straight lines – when I look at the above two comparisons explaining the rise, then the fall and now the sideways price action, the secular case for Gold remains intact. Recent price volatility is entirely down to technical action and profit-taking by traders. There is no basis to suggest the gold run has come to an end. There is a great deal of psychology at play and, as with most securities, it’s a battle between Market Technicals vs Market Fundamentals. The latter determines the long(er) term; the former represents pauses in price behaviour (e.g. profit-taking and adjusting hedge ratios). They are not an “either/or” situation.

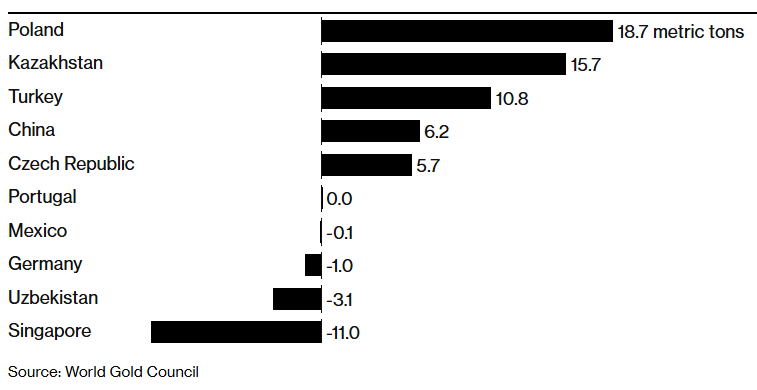

The biggest driver so far of the gold spot price has been Emerging Markets (EMG). Look at the chart below showing the biggest changes in their gold holdings in Q2 of this year. Three standout nations are Uzbekistan, Ghana and South Africa. Uzbekistan is both a major producer as well as a major holder of the metal in its reserves. South Africa is having a great year. It is home to some of the deepest mines and stocks are on track for the best year in two decades (Sibanye Stillwater, AngloGold, Gold Fields have tripled in value) – it is a major producer and the Rand is at a 1-year high while the JSE has gained over +30%. Its 10-year government bond has recently fallen below 9% for the first time in over seven years! Slowing inflation is allowing its CB to cut rates. Ghana is on a path to recovery with the Cedi having strengthened almost +40% this year (Moody’s even upgraded its credit rating). Investors are also keeping a close eye on Poland, Turkey and Kazakhstan – all of whom have been adding to their gold reserves.

What’s driving the above?

At a fundamental level, quite simply politics – based on structural, geopolitical and financial factors! EM CBs are executing a strategic de-dollarisation and reserve-stability shift (aka: the US$ debasement trade) and the freezing of Russia’s $300bn in reserves (back in 2022) was the turning point. It was a wakeup call, a playbook in “look what could happen to you”. It made them realise how foreign-held US$ reserves (and to a lesser extent €-denominated assets) can be weaponised. Gold is outside the clearing system (just like Bitcoin – and why I think this time could be different for BTC). China, India, Turkey and GCC states are building parallel reserve systems centred on gold, CNY and regional currencies. The true weapon of war today is FX – and the US$ has led this war for decades. Now, EMs – led by China – are trying to counter this. China is increasingly seeking settlement in CNY to bolster its share of trade as well as swap lines (a standing agreement between two nations’ CBs allowing one CB to borrow FX from another issuing CB) to facilitate the maintenance of global financial stability and managing liquidity during market stresses. Currently, the US$ dominates some 88% (based on BIS, 2022) of total swap lines in existence!

So, the above is the fundamental case. What about the technical case? Ultimately, this comes down to speculative positioning. Summarising CFTC data as of 23rd September, Open Interest positioning is as follows:

| Trader Group | Long % | Short % | Implication |

| Non-Commercial

(Speculators = Hedge Funds & large Speculators) |

62.9 % | 12.5 % | Dominant long holders (strongly net long – speculators are heavily bullish) |

| Commercial

(Hedgers = Producers, Refiners, Bullion Banks – hedging physical exposure) |

15.7 % | 72.1 % | Primary short side (deeply net short – quite normal for producers hedging high prices who short-hedge into price strength) |

| Nonreportable

(Small Traders = those below reporting thresholds) |

10.9 % | 4.9 % | Minor influence (modestly net long and currently of minor influence) |

Bottom line: (1) positioning remains bullish but not extreme, (2) liquidity is expanding and (3) gold remains in a mature bull phase but is still supported by macro fundamentals. However, it is vulnerable to sharp corrections should speculative longs start to unwind. What could cause that? It would take a combination of three things:

- Prove it is winning the battle to deal with its ever-rising rising fiscal deficit (which, in turn, is adding to its ever-rising total debt).

- Ensure it has inflation under control.

- Reassure the world the US$ can be trusted again as a store of value and not be used as a weapon!

Even if succeeds with points 1 and 2, I think it is past the point of no return on point 3.

MARKET SUMMARY...