Since the joint US-Israeli (US-I) strikes on 28th February, the conflict has moved from the initial shock phase into a broader regional escalation phase. To put it bluntly, this war is not proving straightforward. Some key developments to note:

- The initial objective (leadership decapitation and strategic infrastructure degradation) has not immediately translated into political collapse inside Iran. In fact, on the leadership front, the new elected leader is (as expected) the son (Motjaba Khamenei) of the former Ayatollah. He is a hardliner and has vowed to keep blocking the Straits of Hormuz.

- Iranian retaliation has expanded across the region through the use of hundreds of missiles and drones targeting locations in the UAE, Bahrain and other Gulf states that host US forces. This reflects a classic asymmetric response strategy i.e. instead of confronting USI airpower directly, Iran is attempting to expand the conflict geographically and economically.

- Disrupting the Straits of Hormuz: this is strategically the most important development since last week given that the maritime chokepoint is responsible for some 20% to 30% of all global oil shipments. Iranian action has effectively halted – at least severely reduced – tanker traffic through the Straits. Several tankers have been damaged while maritime insurers have sharply increased war-risk premiums. Oil price action clearly demonstrates markets are trading geopolitical risk – not just pure supply!

- Energy infrastructure is not only a target but has become a central battlefield (e.g. the attack on Saudi Arabia’s Ras Tanura refinery). Strikes linked to Iran have also hit Omani ports, fuel storage facilities and tankers operating near Gulf shipping lanes.

- It has turned into a Regional war spanning the wider Gulf – reaching as far as Azerbaijan and Turkey.

Market action has not moved in a straight line. Instead, it followed the conflict narrative i.e. surging on escalation signals and retreating on de-escalation signals. History shows not every escalation becomes a macro regime shift. Much depends on whether energy prices stabilise from here (as Trump is trying to achieve by quickly paralysing Iran) or whether they continue climbing (as Iran is trying to perpetrate via the Straits). There are two factors working at the same time here:

- The first, is the immediate (cyclical) price spike in in energy. This is a short-term transmission mechanism that saw the oil price rise from high-$60s to $85 pb. This has an immediate impact on retail fuel prices (gasoline, diesel) which results in temporary, inflation pressure. Why do the likes of gasoline move faster than crude? Because consumers do not buy crude… they buy refined fuels. To go from crude to refined is a process along the value chain.

- The second, is the structural (long-term) impact on economies linked to energy-intensity i.e. how sensitive is an economy to oil prices (e.g. cars are far more efficient today in their energy consumption vs say 10 years ago). Consequently, the energy price rise needed to cause pain is much higher. This “oil intensity of GDP” has fallen sharply over the last two decades. The share of energy in the inflation basket is far lower today (US: 6% to 7%) – so it takes a more substantial rise in energy to cause hurt!

Both these impacts reinforce each other. Gasoline & Diesel prices are up +25% and +40% respectively in the US (despite being fully self-sufficient in oil and an exporter since 2023). This is all about the speed of the move. This will feed through into the March inflation report that will be published in April. The other issue is persistence…..and this is all about the impact on energy-intensity. Oil at $85 pb for a few weeks has a minimal impact on pushing inflation BUT it stops inflation from falling (to the frustration of Central Bankers); oil at $85 pb for 3m to 6m adds some +0.3% to headline inflation. If sustained at $100 bp, it adds +0.5% to +0.7% to headline inflation. If sustained above $120 pb….we are looking at an inflation shock! The table below summarises how these two factors (short-term, column 2 and long-term, column 4) reinforce each other depending on the price of oil:

| Brent Oil Price | Short-Term Retail Fuel Impact | Headline Inflation Impact (3–6 months) | Structural Inflation Risk | Impact Given Lower Energy Intensity |

| $60–70 | Stable gasoline/diesel prices | Neutral / slightly disinflationary | None | Economy easily absorbs; energy costs declining share of GDP |

| $75–85 | Gasoline rises modestly (10% – 20%) | +0.2–0.4 pp | Minimal | Services-heavy economies cushion the impact |

| $90–100 | Noticeable fuel increases (20% – 30%) | +0.4–0.7 pp | Possible disinflation slowdown | Structural energy efficiency prevents broader inflation spiral |

| $105–120 | Sharp diesel/gasoline increases (30% – 50%) | +0.7–1.2 pp | Rising risk of pass-through into core inflation | Economy feels pressure but less severe than previous decades |

| $120–140 | Severe fuel shock; logistics costs surge | +1.0–1.8 pp | Significant inflation risk | Energy intensity dampens but cannot prevent macro impact |

| $150+ | Extreme fuel spike | +2 pp or more | High risk of stagflation | Structural efficiency delays impact but cannot offset shock |

Markets are being battered by three forces: (1) events in Iran, (2) the fears and stress of the impact of AI on the labour force and (3) rising concerns in private credit markets (e.g. latest news from Bloomberg is that Cliffwater’s flagship $33bn corporate lending fund is believed to be facing redemption requests exceeding 7% of its value; FT reports JP Morgan is believed to be marking down the value of specific loans held by private credit groups that serve as collateral for bank financing; Swiss entity Partners Group has forewarned private credit default rates could double in the next few years on the back of AI-driven economic upheaval). Even if energy prices stabilise at current levels ($95 – $100 pb), they will still be some 45% higher than when the conflict started. It’s the volatility around the pricing – not the absolute level – that feeds through into volatility around credit spreads… and the latter determines risk premium and subsequently valuations.

MARKET SUMMARY...

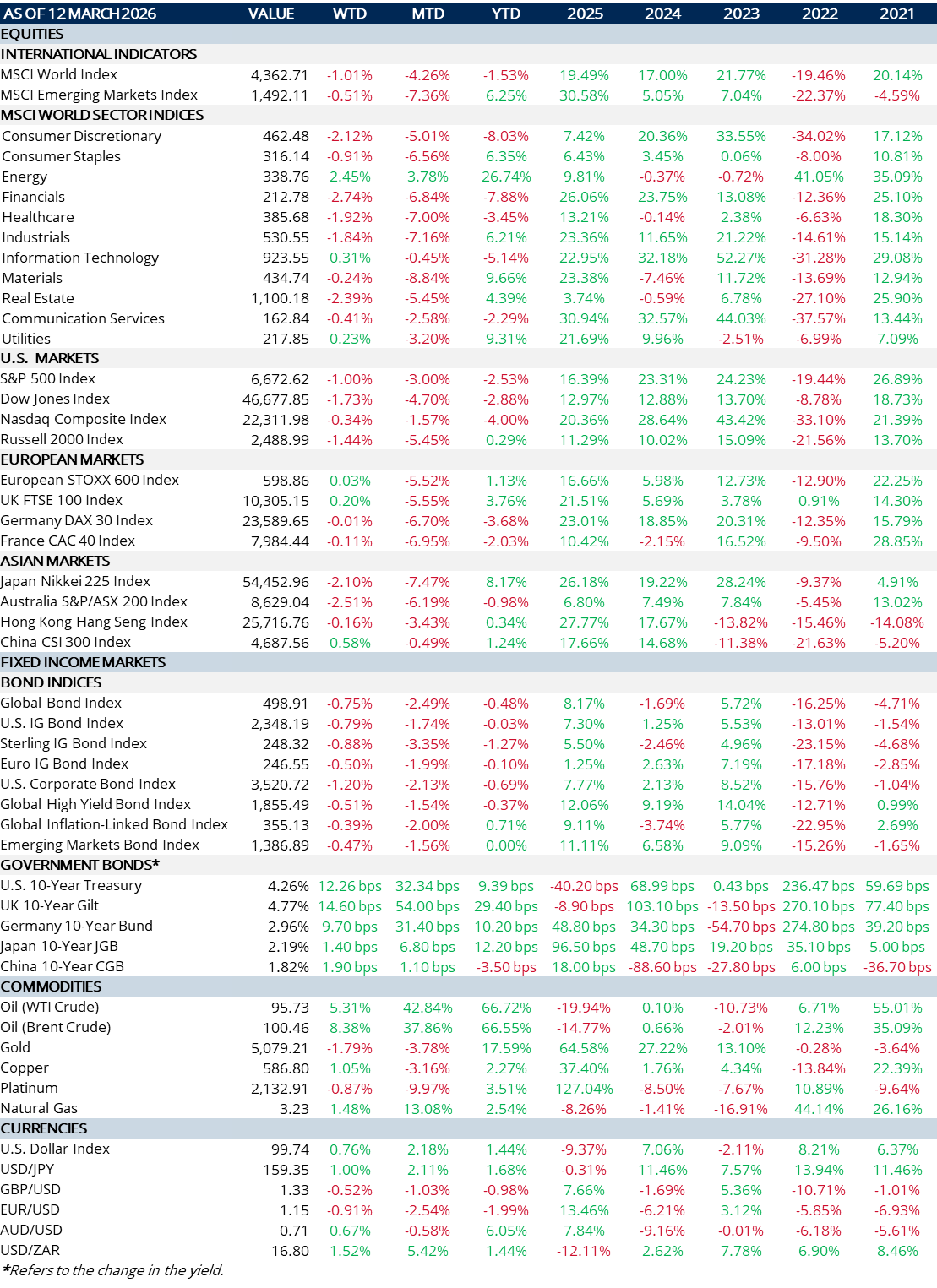

- It’s been more of the same as last week – Risk Off; Risk On and then Risk Off again.

- US$ and Energy up, Equities and Bonds down. Gold hasn’t woken up – yet.

- The US$ trade-weighted index has crossed back above 100 and currently stands at 100.08.

- Inflation is now becoming a real concern – its impact is spreading beyond energy costs and reaching fertilisers and hence food. Thus the above caption (“economic consequences can travel way further than the missiles that started it”).

- The sharp rise in bond yields is concerning and tends to be the straw that breaks the camel’s back. If it happens, gold will fly. In the US, the 30y mortgage rate now stands at 6.35% (from 6.14%) on the week. In the UK, it has already topped the Liz Truss fiasco!