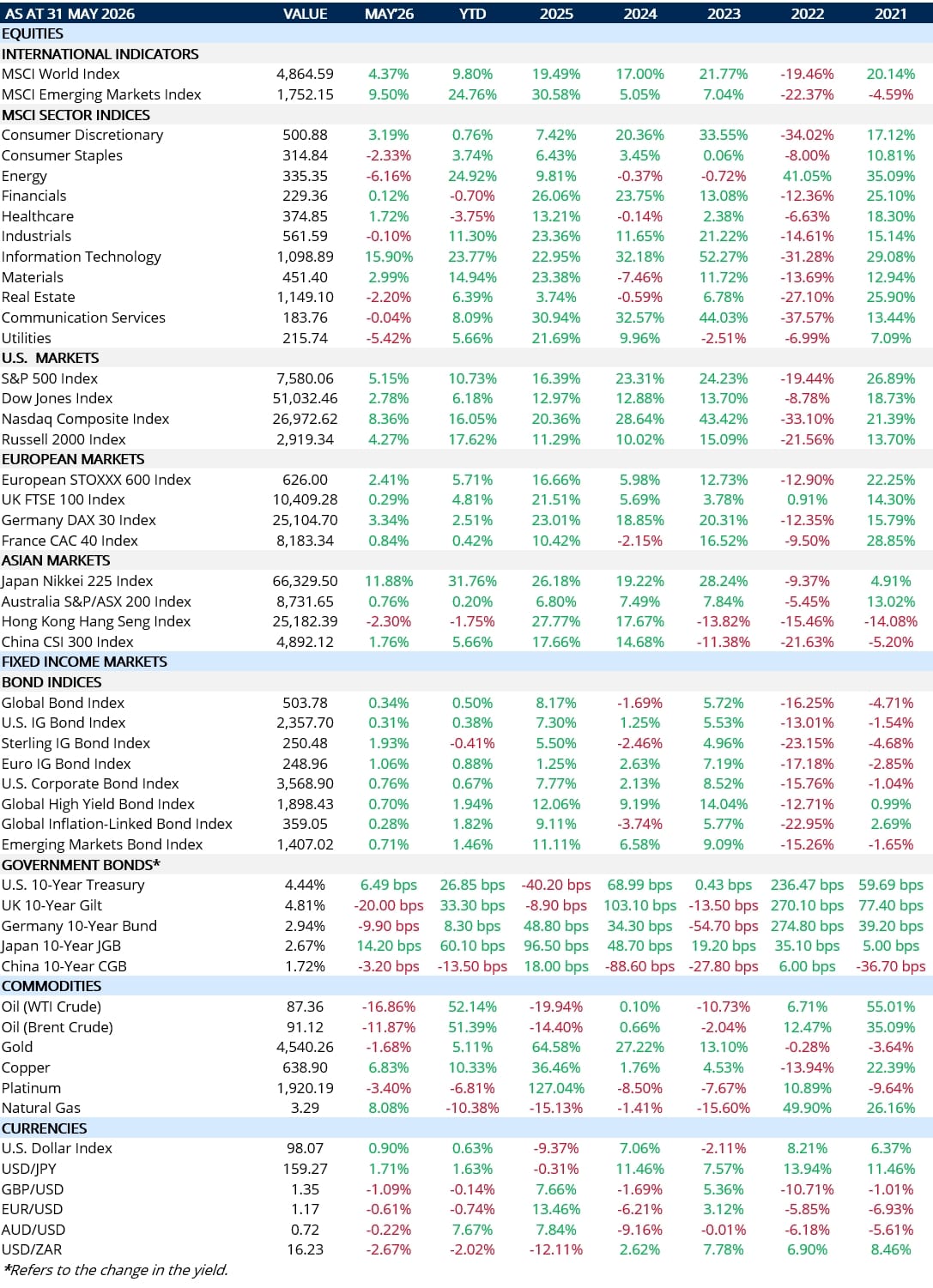

“Sell in May and go away”…….I hope you didn’t!

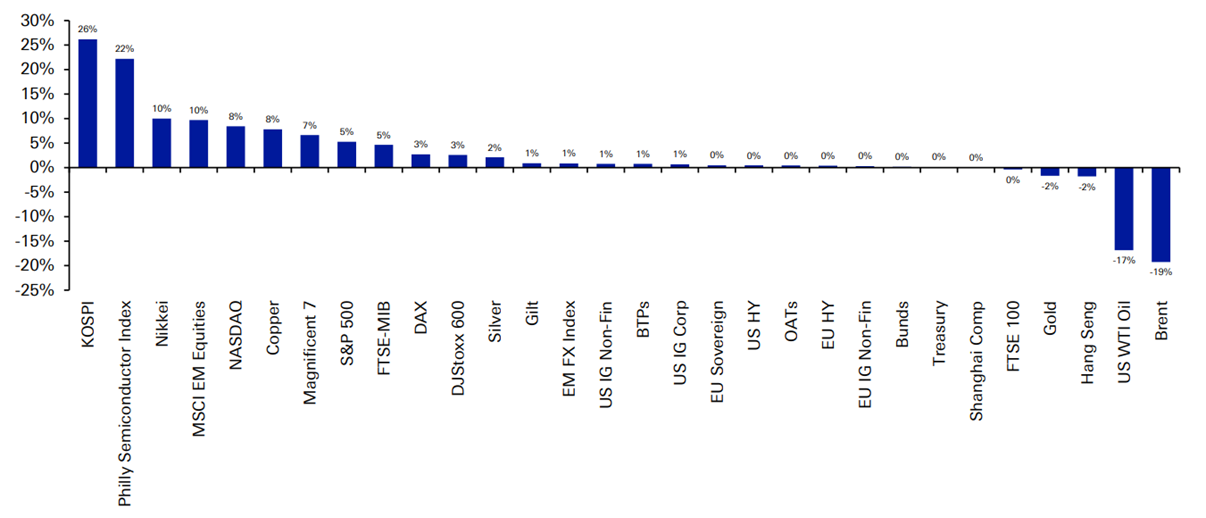

The above saying dates back to high-society London (between 1694 and 1776) when wealthy investors and brokers would leave the city for their country estates and summer holidays. If you did then, on this occasion at least, it would have cost you dearly. The chart below (courtesy of DB) shows May 2026 performance (in US$ terms) for select, global assets:

A more detailed performance breakdown is given in the table at the very end but, May’s performance, was in three parts and followed the trials & tribulations of progress around a US-Iran peace accord. The first was 6th May when we were (apparently) close to end of war resulting in a sharp drop in oil prices ($114 pb to $100 pb) the next day. There was also another upward boost in payrolls. The second was when Trump posted a comment saying Iran’s counter-proposal was “totally unacceptable”. Together with a strong inflation print, bond yields hit multi-year highs. The US 30y Treasury hit 5.18%, the German 10y hit 3.19% and Japan’s 10y hit 2.78%. The third saw a return to optimism on the back of suggestions US & Iran were close to a deal again. Oil hit a 1m-low, equities had a great run and yields kept falling. To cap it all, AI frenzy returned as chip stocks massively outperformed:

- The Philly Semiconductor index rose +22% (YTD = +82%).

- The KOSPI (Korea) index rose +26% (YTD = +94%; over +100% in local FX).

……and this AI frenzy seems to be outweighing everything else right now! May’s performance would suggest the world had become a safer place. Global equities have climbed to fresh highs, credit spreads remained near historically tight levels and investor confidence continues to recover. At the same time, Brent Crude remains elevated (still well above its pre-28th Feb. level though it has retreated from its $100 to $110 pb range), inflationary pressures continue to build and bond yields remain stubbornly high. The Iran conflict still continues – not forgetting we have seen fresh attacks (again) by the US on Iran, Iran on US bases in the Gulf (in retaliation) and further incursions by Israel into southern Lebanon. The latter is arguably the primary reason the US can’t strike a deal with Iran and is rumoured to be the source of major tension between Trump and Netanyahu.

Something doesn’t add up here! Either equity markets are correct in concluding strong earnings growth and the AI investment boom can comfortably absorb the inflationary effects of higher energy prices or bond markets are correct in warning us inflation is still unfinished business! Economic history says they can’t both be right. If so, which one gives? The table below attempts to dissect this (using the S&P 500) based on movements in earnings and yields:

| Scenario | Key Assumptions | Supporting Evidence Today | Fair P/E | Implied S&P 500 Fair Value* | Upside / Downside |

Goldilocks / AI Wins |

AI capex boom continues; inflation fades; bond yields ease | Q1 EPS growth +29%; EPS beat rate 84%; AI investment >$800bn; Brent falls back towards $80 | 31.1x | 10,900 | +44% |

| Current Market (What Equities Are Pricing) | EPS growth remains at about 20–25%; inflation rises modestly but remains contained; yields stabilise around current levels | Q1 EPS +29%; revenue +11%; EPS beat rate 84%; Brent $94; US 10Y 4.45%; earnings revisions near historic highs | 21.6x | 7,665 | +1% |

| Inflation Sticky | Oil shock feeds through to freight, wages and goods prices; inflation proves persistent; yields rise to about 5.0% | Brent remains near 91st historical percentile; US real yields remain above 2%; bond market continues demanding inflation compensation | 15.7x | 5,495 | -27% |

| Oil Shock / Risk Premium Rises | Middle East escalation persists; oil remains elevated; inflation reaccelerates; bond yields move above 5.25% | Oil supply disruption extends; inflation pipeline fully feeds through; equity risk premium rises from unusually low levels | 12.7x | 4,445 | -41% |

What we have witnessed thus far, is a bullish Q1 2026 S&P 500 earnings growth tracking at +26% y/y. Contrast this with a consensus of +12% and a median of +14%. Following these earnings releases, analysts have revised their forecasts upwards. Lipper has it higher at +29% y/y. It forecasts earnings growing at +22% in Q2, +24% in Q3 and +23% in Q4. On a forward looking 12m outlook, it values the S&P 500 at 21.6X – expensive but justified on these earnings growth projections. Four categories skew the results: IT (+54% y/y), Communication services (+49% y/y), Consumer Discretionary (+41% y/y) and materials (+42.5% y/y). Furthermore, within those sectors, Nvidia, Microsoft, Amazon, Alphabet and Meta are responsible for a disproportionate amount of this growth. In other words, the market is not pricing broad, economic strength – it is pricing AI-driven strength. For the bond market, this is a problem! Right now, the market can sustain a valuation of 21.6X forward P/E (Price to Earnings ratio) provided yields (US 10y Treasury) stay at around 4.5% AND Earnings grow at 20% to 25% y/y. However, the minute yields start to go higher, that forward valuation starts to diminish. As a guide, a yield of 4.0% equates to a fair P/E of 24X to 25X; at 4.5%, it is 21X to 22X; at 5.0%, it is 18X to 19X; at 5.5%, it is 15X to 17X.

In summary:

Investors find themselves caught in a tug-of-war. Markets have not ignored the Iran war – rather they have concluded earnings growth remains powerful enough to offset it. Refinitiv’s latest earnings update shows companies continue to beat expectations. However, bond markets are sending a different signal – the US 10y yield is near its 94th percentile of history while Brent remains in the 91st percentile. Equities are looking through the geopolitical noise and pricing for growth with a focus on earnings; bonds are looking through earnings and pricing for inflation. The outcome of this battle will determine not only the direction of markets during the second half of the year but also whether the current rally has further to run or is simply living on borrowed time!

| Current Reality | Future Risk |

| Earnings: +26% | Consumer spending is expected to slow |

| Revenues: +6.3% | Margins are under pressure |

| Spending: still healthy | Inflation pipeline is still building |

| AI capex: exploding | Oil shock is not yet fully transmitted |

MARKET SUMMARY…