Following some of the major elections held last year, here’s a quick take on how things are shaping up for the new players in town:

US: Based on the latest RealClear polling, the table below summarises current, voter opinion in the US:

| Favourable (%) | Unfavourable (%) | Swing (%) | |

| President Trump | 44.2 | 52.5 | -8.3 |

| Republican Party | 41.5 | 53.5 | -12.0 |

| Democratic Party | 34.7 | 59.0 | -24.3 |

| 2026 Generic Congressional Vote | Republicans = 43.2 | Democrats = 45.8 | 2.6% (in favour of the Democrats) |

The fall, in Trump’s own approval rating, should not come as a surprise given the turmoil both the US and the RoW have been through – most notably – given the tariff and immigration sagas. The mid-term elections are going to be key – but there is no use fretting over them just yet. They are still over a year away. Fyi, even over the past month, CNN polling has shown an improvement of between +1% and +2% in Trump’s approval rating – that’s how fickle voters are! I certainly don’t think Trump is losing sleep over it and, what’s more, his campaign team will know exactly what needs to be done to get it back over 50% (53% during the 5th to 7th of February). What’s even more interesting is how disastrously the Democrats are faring – and this despite tariffs, immigration and the government job layoffs! They do not have anything or anyone to fire back against Trump. Both Kamala Harris and Gavin Newsom have said they will consider running for President in the next (2028) election – in Newsom’s case, he will wait till the outcome of the midterm elections next year i.e. let’s see how we are doing before I make a fool of myself.

When you dig below the surface, the main concern voters (still) have is around inflation, specifically core services inflation that affects their household bills. An IPSOS poll (10th Oct. 2025) found 69% of Americans are spending more on food to cook at home and less on experiences like travel or dining out in the past six months. By age group, it is even higher among the 18y-34y group (76%) and 35y-54y (75%) vs the 55+ group (58%). In a poll conducted 26th Sep. 2025, 48% said they do not have money left for the things they want, up +7% from May 2025. 45% are reporting they worry about paying all of their bills each month, +5% from May 2025 and +10% from April 2024! These were the same issues in existence during the Biden administration. Trump’s pledges to bring inflation down helped him to get elected. A 15th September poll showed 90% of Americans saying there is an urgent need for greater unity among Americans. This poll was conducted shortly after the killing of Charlie Kirk. 92% disagree it’s acceptable to use violence to achieve political goals. When you put all this together, you can see why polling puts the Democrats slightly ahead of Republicans for Congress – it’s the electorate’s way of enforcing governance.

Therefore, ahead of the midterms, Trump needs to step up efforts around inflation. September inflation of 3% y/y was a relief to economists and markets…..but it misses the point for two reasons: (1) it was heavily distorted by a much lower-than-expected rise of just +0.13% in OER (Owners’ Equivalent Rents, indirectly an expense associated with home ownership that includes insurance, Home-Owners Association fees, property taxes and maintenance). OER is has a 44% weight in the Core Services CPI (which dropped to 2.9% y/y) and 33% in the Core CPI (which dropped to 2.8% y/y) and (2) the inflation that hits consumers is the one that’s really hurting them i.e. groceries, housing (OER) and insurance. These are running well above 3%. The above comment that “…..they do not have money left for the things they want…..” essentially describes why consumer sentiment has fallen. Some examples of annual price changes include Coffee +18.9%, Beef & Veal +14.7%, Bananas +6.9%, Frozen Fish/Seafood +6.6%, Food from vending machines +6.3%, Utility Gas (piped) bills +11.7%. These are not entirely down to tariffs…..but tariffs will add to it whatever the final rate is. A 17th Oct. analysis (by Yale) concluded the current tariff policies in place will cost each household $1,800, on average, in 2025.

GERMANY: The new Chancellor, Friedrich Merz (FM) is not finding life straightforward. He has tried to assert himself abroad (Ukraine and the US as well as across Europe) but at home, German impatience is growing. The new government in Berlin has loosened the purse strings to address an economy that has been stagnating for the past 3 years. Employment numbers have been contracting sharply with 245,000 jobs lost in industry since 2019. A spending plan of €500bn over the next 12 years was assembled (securing SPD support) to try and fix the country’s crumbling infrastructure. However, growth is still only expected to be 0.2% this year. Steel output is down -12% annualised and car manufacturing is down from 6mn (2017) to 4mn today. Tariffs have not helped matters.

A recent poll by Insa has two-thirds of Germans saying they are dissatisfied with the ruling coalition (+20% from June). Worryingly for FM is that the AfD (Germany’s so-called Far-Right) party has risen from a 21% share of the vote in the last election to latest polls (Politico) putting it on 26%. It now leads over the CDU/CSU as the single, largest party. It has even tripled its vote share in North Rhine-Westphalia (Germany’s most populous state) where it ate into the SPD’s vote share. Unfortunately for FM, he faces challenges even from within his own party e.g. over the debt brake (0.35% of GDP). The latter was relaxed for infrastructure and defence but remains in place for everything else. This has opened up a budget gap of €30bn. Five Federal states hold elections next year and these include two former communist states – one CDU ruled and the other SPD ruled – the AfD is predicted to win both! That will eat even further into the slender 13 seat majority of the current ruling alliance (CDU/CSU and the SPD).

FRANCE: From one mess to another…..Prime Minister Lecornu (the 4th PM under President Macron) announced a draft budget two weeks ago which looks to make a saving of €30bn…..vastly reduced vs what was originally proposed. MPs are set to hold a crucial budget vote on 4th November and it’s unlikely there will be a consensus. Lecornu already tried to resign once – but Macron asked him to try again. The reality is clear: the French electorate want Macron to resign even though this is his last term ending in 13th May, 2027.Lecornu has survived two no confidence votes (by just 18 votes). The budget has been watered down several times – the most significant reform was the gradual increase in the retirement age from 62 to 64 and this has been removed. It’s costly (some €2bn over two years). On the one side, the leftists are making heavy social demands while on the other, the far-right are blocking any move he makes. The far-right (The National Rally) is anti-tax and pro high social spending. The centre-right wants all tax increases to be kept to a minimum. The socialists are struggling to accept the spending cuts. The left are also trying to force a 2% wealth tax (annual levy) on all fortunes over €100mn. France’s budget deficit currently stands at 6.1% of GDP, far in excess of the 4.6% target submitted to the EC. The draft budget was aiming for 4.7% but Lecornu has now softened the target to “below 5% of GDP”. I suspect the final outcome will be above 5%. In the final instance, Lecornu could try and enforce Article 49.3 which would allow him to impose a version of its original budget by decree! This has never been done before and would for sure result in his removal if it happened. Alternatively – perhaps additionally – if new elections are to be held, this MUST happen before 15thNovember due to rules dictating election lengths and emergency budgets. They have to allow at least 20 days between dissolving the chamber and the first round of elections and at least 35 days before the second round of elections. Meanwhile, latest polling places Marine Le Pen’s far-right RN (Rassemblement National) winning with 34% of the national vote (as of 8th October) – unchanged from 1st May. Happy days ahead!

UK: At least in France – and Germany – you can understand why things are at loggerheads given that both governments are built on alliances and coalitions. The UK has no excuse! With 411 seats, Starmer’s Labour party has an outright majority of 86! Yet over a year later, its ability to govern has been a shambles. We have had government reshuffles, scandals and rapidly declining confidence in industry and commerce. Last year’s budget was toxic resulting in yet another black hole in the budget (estimated to be between £30bn to £40bn). Tepid growth has meant bond yields have been rising resulting in higher debt-servicing costs (over £100bn pa in interest). The next budget (26th November) is make or break for the country. Consumer spending has kept the economy afloat so far but tax burdens are rising and it is debateable how long this can continue. Opinion poll after opinion poll has The Reform Party polling between 27% and 35% while the other parties (Labour, Conservative, Greens, LibDems) are hovering between 15% and 17% each. Based on this polling, Reform would secure around 324 seats, just 2 shy of an outright majority! Other polls suggest far more than this.

Growth is expected to average +0.2% for each of the next four quarters with an overall +1.3% to +1.4% this year. The unemployment rate is expected to hit 5%and inflation 3.8%. While interest rates are expected to be 4% by year end, 10y yields are expected to be around 4.65%. Perhaps one reason the consumer has managed to buoy the economy so far is the debt deleveraging that has taken place – household debt to GDP is the lowest since 1995! The challenge is for the government to get policy sorted to take advantage of any capacity to borrow further for growth. The labour market is giving mixed signals – perhaps due to businesses adapting to changing taxation policy. Overall, the consensus vie wis that the labour market will be flat. Food and energy prices have been a big knock to household inflation (e.g. food inflation is running at 6%) while service sector average earnings are 4.4% pa (far above CPI). It will have to be a neutral budget on households, friendly for businesses while raising new revenue streams fairly.

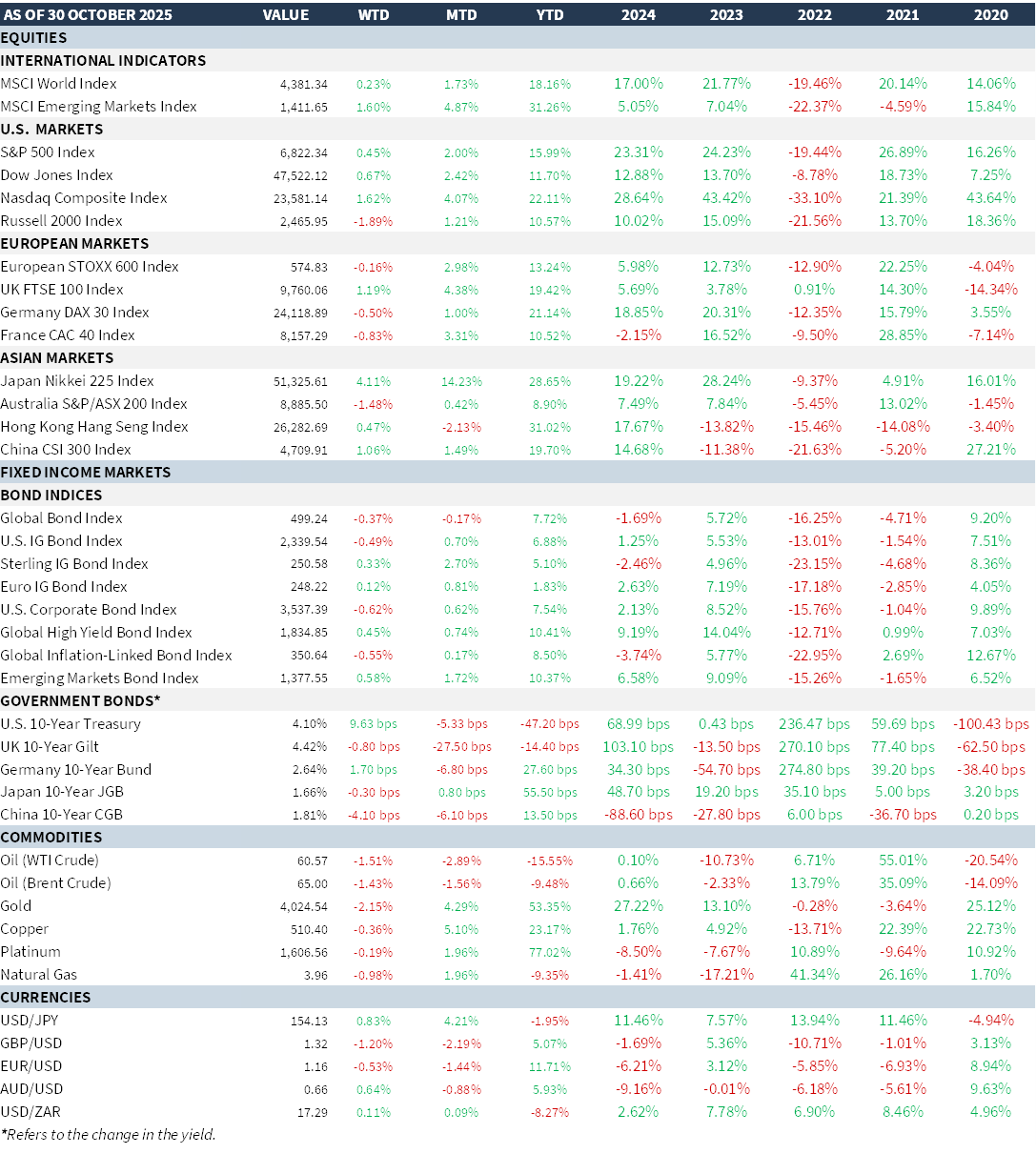

MARKET SUMMARY...