Dear All,

Deal………….or no deal?

As of this (Friday) morning, the planned Switzerland meeting to sign an interim agreement has been cancelled. No replacement date has been set yet. The reasons are threefold: (1) Iran wants to see evidence the US is implementing its actions before sending its negotiators for signing; (2) Israeli military activity continues in Lebanon and (3) all this has resulted in domestic political backlash in both Israel and the US as the agreement is seen as being very one-sided in favour of Iran. None of this means the deal is dead – but it has stalled. The agreed interim Memorandum of Understanding (MoU) between the US and Iran still stands and provides a framework for future negotiations – not a final settlement. Here’s what we know about the proposed agreement so far:

| Area | What Appears Agreed | Investment Significance |

|---|---|---|

| Military Conflict | Formal cessation of hostilities and extension of ceasefire arrangements | Removes immediate war premium from markets |

| Strait of Hormuz | Reopening of shipping lanes and restoration of commercial traffic | Bearish for oil prices |

| US Naval Blockade | Blockade of Iranian ports expected to end | Additional crude supply returns to market |

| Iranian Oil Exports | Sanctions waivers and resumption of exports appear likely | Increases global oil supply |

| Nuclear Negotiations | 60-day negotiation period established | Core issue postponed, not resolved |

| Frozen Assets | Partial release under discussion | Economic relief for Iran |

| Sanctions Relief | Phased and conditional | Dependent on compliance |

| Reconstruction Package | Large Gulf-backed reconstruction fund reportedly being discussed (rumoured to be $300bn) | Regional stabilisation incentive |

| Ballistic Missiles | Not included — deferred | Major unresolved issue |

| Hezbollah / Regional Proxies | Not included — deferred | Major unresolved issue |

| Iranian Uranium Stockpile | Not resolved — deferred | Biggest remaining obstacle |

The US – especially VP Vance – is defending the deal strongly within GOP ranks as well as towards Israeli cynics. My cynical take is that this is just a strategic pause for the following reasons:

- The Midterm Elections: Historically, US voters are extremely sensitive to petrol prices, inflation and cost of living. If Brent had stayed above $100 to $110 pb with gasoline prices staying materially higher, the Democrats would have had a field day. At the time of writing, Brent has fallen below $80 pb. Trump can now spin this as a peace deal with oil prices coming down – even though the reality is they are simply where they were before the start of the war!

- Rebuilding of the Strategic Petroleum Reserve (SPR): a key reason oil prices did not go any higher (above $110 pb) was due to the dampening effect of releasing vast amounts of oil from reserves. The latter has to be replenished and a calmer oil market is the best time to do this.

- Israel Needs Time Too: Despite Israel’s military success, it needs to rebuild missiles and munitions. Historically, Israel has fought in stages rather than continuously. There is undoubtedly disappointment back in Israel given the mismatch between what Israel thought it was fighting for and where things have been left are miles apart (e.g. permanent dismantlement of Iran’s nuclear programme, potential collapse of the Iranian regime, strategic weakening of Hezbollah, seeking an unconditional alignment of US support). Instead, the outcome to these has been left unclear or has failed.

- Iran Gets a Breather: this is arguably the biggest objective from the Iranian side. It most likely needs hard FX, oil export revenue, infrastructure repair and domestic stabilisation. The regime may well have exchanged strategic concessions for survival time.

- Markets Were Part of the Problem: Inflation à Bond Yields à Equity Valuations à Credit Conditions. In one go, a ceasefire removes a large part of this pressure. The US today is much more sensitive to asset prices than it was 20 years ago.

- Kick the Can Down the Road: this is Trump’s characteristic negotiating style i.e. create leverage à escalate pressure à declare victory à sign framework agreement à extend negotiations. Sometimes, maintaining leverage is more valuable than seeking permanent solutions.

- China: imports roughly 11 to 12 mbpd of oil. She is the world’s largest energy importer and benefits enormously from stable Middle East supply, lower oil prices and open shipping lanes. Hard to see why Beijing wouldn’t be happy with a negotiated pause – I wouldn’t even be surprised if this has its roots in the meeting between Trump and Xi a few weeks ago?!

To summarise the above:

| Official Narrative | Cynical Interpretation |

|---|---|

| Peace deal | …aka Strategic pause |

| De-escalation | …aka Rearmament and replenishment |

| Diplomatic breakthrough | …aka Temporary political convenience |

| Lower oil prices | …aka Inflation management |

| Regional stability | …aka Risk premium removal |

| Nuclear talks | …aka Kick the can down the road |

What does all this mean for markets? More than likely, the original narrative has changed. The next 120 days are critical as they take us to the US mid-term elections. The base case (Goldilocks) sees its odds drop from over 50% to under 50%. It can be salvaged assuming a ceasefire can be negotiated between Israel and Hezbollah! The growing risk now is Sticky inflation / Rising yields combined with a more Hawkish-sounding new, Fed Chair (Kevin Warsh) who chaired his first FOMC. The table below is not an exact science but an indication of trend and direction based on the three most likely scenarios:

| Region / Asset | Goldilocks / Extension Rally (War → Peace) = 45% | Sticky Inflation / Rising Yields (War → Ceasefire → Delayed Negotiations → Further Extensions) = 40% | Renewed Conflict / Oil Shock (15%) |

|---|---|---|---|

| Brent Oil | $68 to $75 pb | $75 to $90 pb | $100 to $130 pb |

| US CPI | 2.5% to 2.8% | 3.0% to 3.5% | 3.5% to 4.5% |

| US 10Y Yield | 4.0% to 4.3% | 4.8% to 5.3% | 5.0% to 5.8% |

| Gold | $3,900 to $4,300 | $4,400 to $5,000 | $5,000 to $6,000 |

| S&P 500 | 8,300 to 8,500 | 6,800 to 7,400 | 5,500 to 6,500 |

| UK Equities | +5% to +10% | -5% to +2% | -10% to -20% |

| Eurozone Equities | +8% to +12% | -5% to +5% | -15% to -25% |

| China Equities | +8% to +15% | 0% to +8% | -5% to -15% |

| Japan Equities | +5% to +10% | -5% to +5% | -10% to -20% |

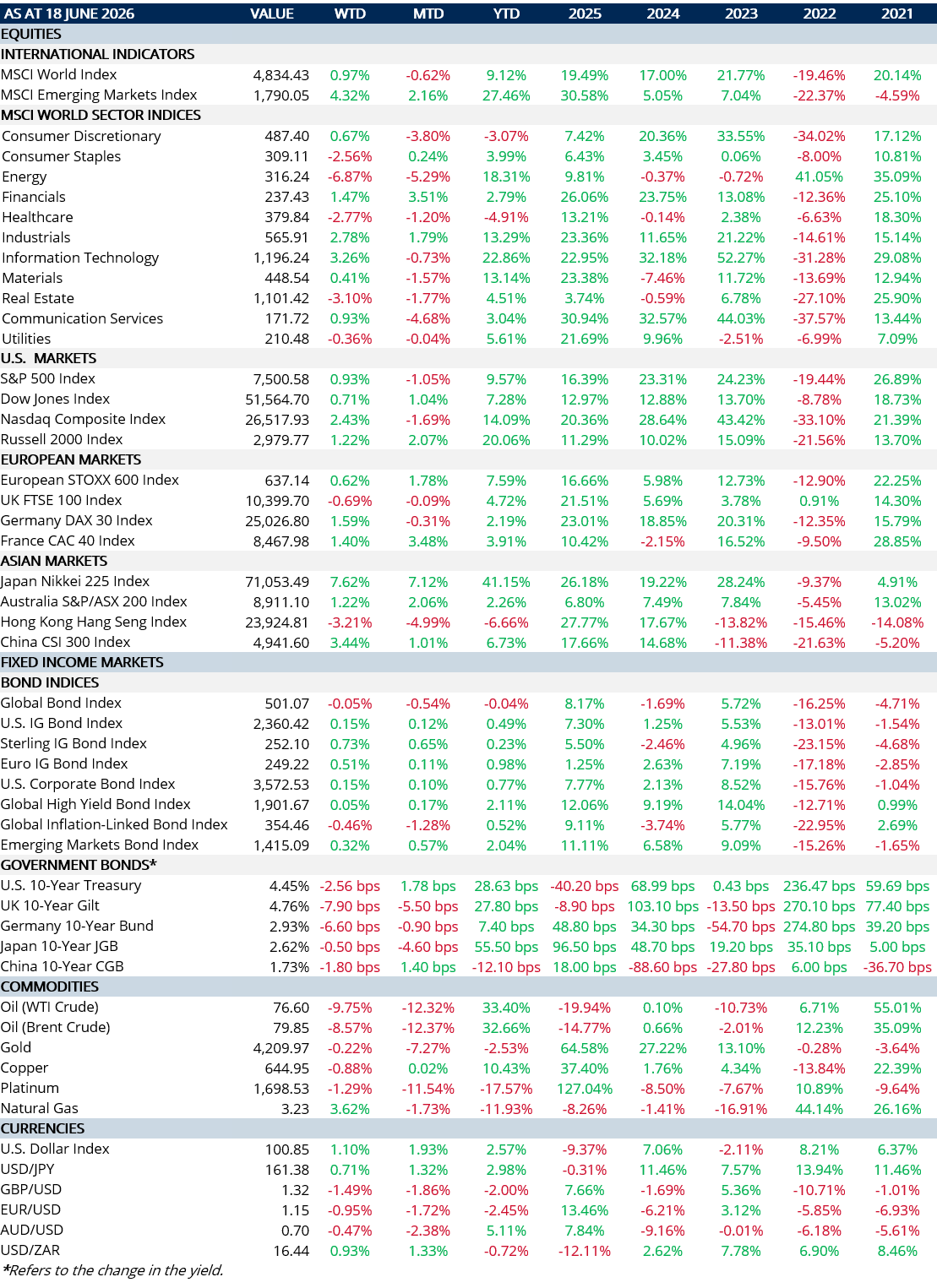

MARKET SUMMARY…

- New Fed Chair Kevin Warsh makes Powell look like a dove! His statement removed any kind of “forward guidance”. He even had his “dot” removed form the conventional “dot plots”. In fact, his statement was short and crisp. Interestingly, he emphasised markets (e.g. bonds) “are probably the most important source of information to guide central bankers”……as “markets are paying attention to what’s happening in the real economy”. He also announced five task forces focusing (1) communications, (2) size and composition of the Fed balance sheet, (3) Fed’s reliance on existing data sources providing often unreliable data, (4) reviewing the Fed’s inflation framework and letting the economy “run hot” as a higher rate of inflation and a hot economy may be the only palatable way of dealing with an unsustainable US fiscal problem more manageable and (5) productivity and jobs in the era of AI.

- Japan’s central bank (the BoJ) hiked rates in their pursuit of normalising monetary policy on a gradual basis. Japanese equities had a great week. The government still wants to maximise GDP. The Yen continues to remain undervalued.

- The US$ had a strong week surpassing the 100 level on a Trade-Weighted basis.