Council elections rarely change governments…..but they can change the mood within the government.

Yesterday (Thursday, 7th May), UK voters cast their vote for Council elections (in England) and Parliamentary seats in Wales and Scotland. For England, local council elections should be about local issues (e.g. schools, libraries, refuse collection) but they rarely are. Instead, they end up being a temperature check over (1) the Prime Minister’s performance, (2) the degree of fragmentation for the ruling government and (3) a proxy war over the ruling party’s leadership. The table below shows what’s at stake:

| Nation | Election Type | Seats / Positions Being Contested | What is being tested? |

| England | Local council + mayoral elections | About 5,066 council seats across 136 English councils + 6 mayors | Labour Party Coalition Fragmentation (to the Reform and Green parties) |

| Scotland | Scottish Parliament (aka Holyrood) election | 129 MSPs (Member of Scottish Parliament) | Labour Party recovery vs SNP (Scottish Nationalist Party) |

| Wales | Welsh Parliament (aka Senedd) election | 96 Members of the Senedd (a new proportional representation system comes into effect) | Labour Party identity erosion; a surge in Plaid Cymru (Welsh Nationalists); Growth in Reform |

The results? See summary set out below:

| Region / Metric | Pre-Election position | Expectation | Actual Result (Latest) | % Counted / Evidence Base | Interpretation / Commentary |

| England — Total Council Seats | 5,066 seats contested across 136 councils | Highly fragmented result expected | 117 of 136 councils declared | 86% of councils declared | Sufficient data now exists for a robust national interpretation |

| Reform UK | Rising challenger party | Major breakthrough expected | 1,313 councillors (+1,311) | Based on 117 councils declared | Reform has moved from protest movement to major political force nationally |

| Labour | 2,200 defended seats | Heavy losses (1,200–1,900 projected) | 823 councillors (-1,180) | 86% declared | Very severe losses; currently toward upper end of “serious” scenario |

| Conservatives | Weak national base | Further losses expected | 661 councillors (-483) | 86% declared | Conservatives weak, but Labour carrying larger political damage |

| Liberal Democrats | Southern tactical strength | Modest gains | 724 councillors (+93) | 86% declared | Continued anti-Tory tactical positioning rather than national breakthrough |

| Greens | Strong urban trend | Significant gains expected | 418 councillors (+298) | 86% declared | Critically important – confirms Labour leakage on progressive flank |

| Independents | Fragmented local presence | Slight decline | 131 councillors (-23) | 86% declared | Independents squeezed by national fragmentation into party blocs |

| Turnout | Historically low locals | Slight increase expected | About 32% estimated turnout | National estimate | Important: this is active voter repositioning, not voter apathy |

| London / Urban Areas | Labour dominant but vulnerable | Green leakage risk | Greens win Hackney + Lewisham mayoralties | Declared | Labour now leaking simultaneously left and right |

| Scotland (Holyrood) | Labour recovery narrative fading | SNP likely largest | SNP 55 seats (-5); Labour 8 (+1); Reform 5 (+5) | 91 of 129 seats declared | Labour recovery appears to have stalled badly; Reform breakthrough now real |

| Wales (Senedd) | Historic Labour stronghold | Plaid surge possible | Plaid 43; Reform 34; Labour 9 | 96 of 96 seats declared (complete) | Politically catastrophic for Labour psychologically (been a Welsh stronghold for over 100 years); Wales no longer safely Labour |

Conclusion: Assessing the damage for the incumbent Labour Party on a scale of Manageable vs Serious vs Existential – this is beyond Manageable and definitely Serious! That said they still have a sizeable majority in Parliament so there is no question of the Labour party voting against itself in a no-confidence motion; they will hang in there till the very end of this term. The issue is no longer whether Labour can defeat the Conservatives – it is whether any party can still assemble a broad enough coalition to govern Britain coherently! As for Keir Starmer – he is definitely wounded – but not yet finished. While these results are probably the worst political moment of his premiership, they are not – on their own – sufficient to remove him. Will he stay or will he go will depend on:

- The next few days/weeks. He has acknowledged that while these results are shocking, now is not the time to step down. Furthermore, there is no organised successor to replace him. Internally (e.g. Angela Rayner, Wes Streeting) – his would-be challengers – are themselves scarred. Externally (e.g. Andy Burnham), they need Party approval first. Also, while the Mandelson/Epstein saga hangs over him, Parliament did vote not to proceed with any further investigation over his handling of Mandelson’s appointment.

- Medium term (6 to 18 months): this depends on whether other parties continue to grow in strength and which path the economy takes.

- To remove a Leader is much slower under Labour – several factions get to vote (members, MPs and NEC).

Any ousting will be a “quiet” and drawn-out affair. The signs to look out for are: (1) MPs asking if he can still lead them to a win (this has started already); (2) the Cabinet distancing itself from him; (3) Organised pressure (e.g. pressure from leading groups and figures like the NEC); (4) Voluntary exit pressure being exerted (that’s effectively what happened to Blair following Iraq); (5) formal leadership challenges (though this comes later). For now, Starmer is precariously safe but very damaged. While leadership speculation has begun, not all his MPs are fully panicking. One it of luck can change everything for him! The conversation inside the Labour party has fundamentally changed to “can Starmer still win the next General Election?” This question requires deep thought and time.

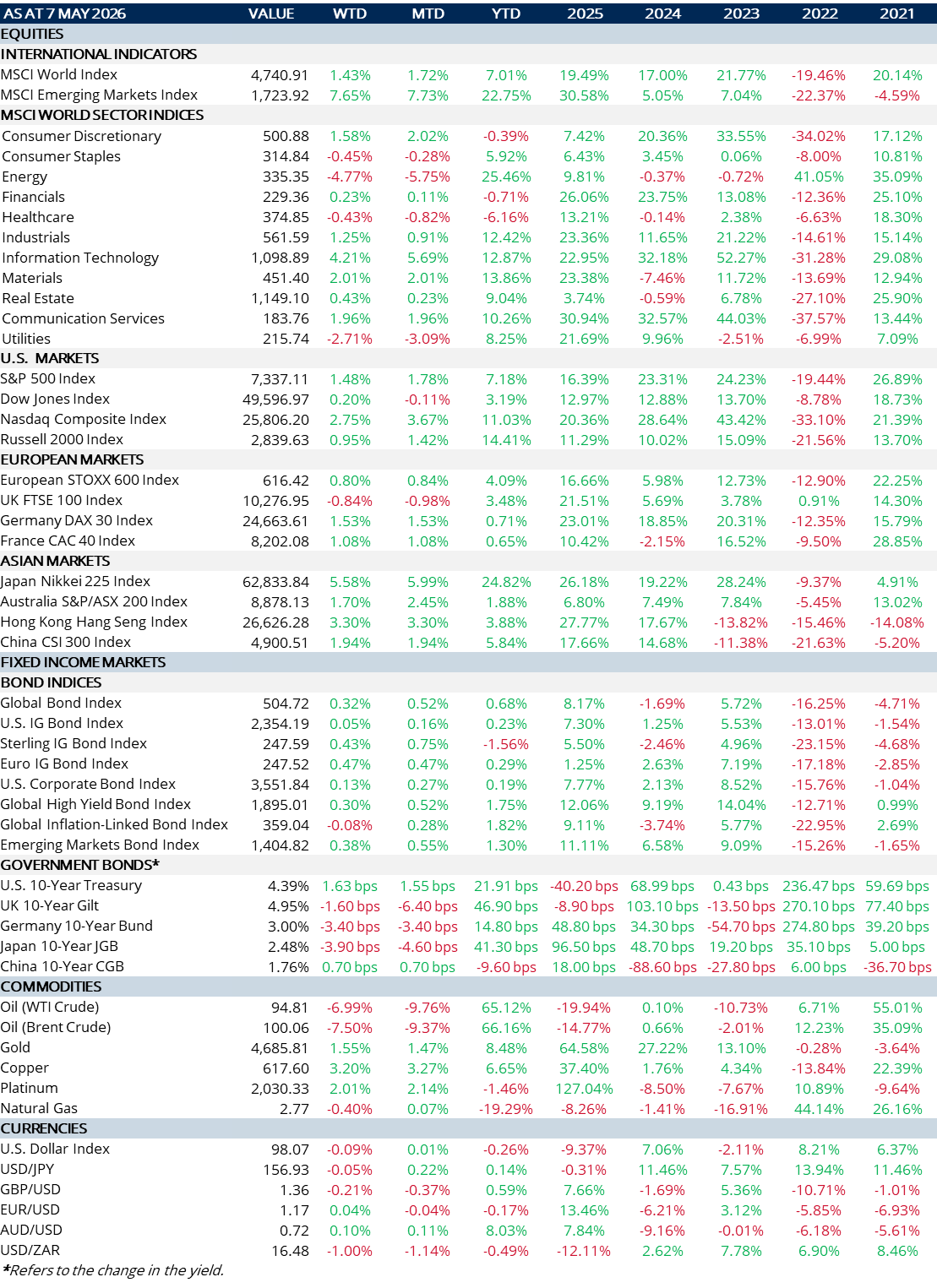

MARKET SUMMARY…

- April’s US Nonfarm Payrolls rose +115,000 (vs March: 185,000), significantly better than the forecast (+55,000). The rise was led by healthcare (+37,000). Transportation & Warehousing added +30,000; Retail gained +22,000. Information Services fell -17,000.

- Average hourly earnings rose +0.2% m/m (=3.6% y/y). Despite a drop in tech-related jobs, the labour market has been holding steady for 12 to 18 months.

- The S&P gained on the back of a strong jobs report and hopes of a deal with Iran. The latter was echoed around most markets, especially EM.

- Consumer sentiment is showing clear signs of weakening with energy costs cited as the main reason. A gallon of regular gas stands at $4.54 – some 40 cents higher vs a month ago.

- EM hard FX bonds have reversed most of their weakness. Flows into hard FX EM bonds have totalled $4.4bn YTD (1stMay).